Want to Get Rich? Buy the Dip on This Dividend-Growth Stock and Never Sell

There are two big schools of thought in investing. In one school, investors focus on growth, buying businesses they hope are much larger five, 10, or 20 years in the future. In the other school, investors search for yield, buying dividend-paying stocks to build passive income and a reliable cash-flow stream for their portfolios. Of course, there are more than just these two considerations when buying stocks, but growth and yield are two of the main factors.

Dividend-growth investing combines the best of both worlds. Dividend-growth stocks are ones that not only make regular cash payments to investors but also have a growing business that can fuel dividend growth over the long haul. The perfect dividend-growth stock might be Visa (NYSE: V), the global payments giant.

Today, you can buy shares for a 10% discount from the stock’s all-time highs set earlier this year. Here’s why now may be the time to buy the dip on Visa stock.

Visa: A take rate on global spending

Visa is a company most of you will know. It is the world’s largest credit card, debit card, and payments network, serving 4.5 billion credit/debit cards as of last quarter. That is up from 4.2 billion in the same quarter a year ago. A huge percentage of the world’s consumer spending runs on the Visa network, from the United States to Europe to emerging markets in Asia and Africa.

The business model works slightly differently than you might imagine. Even though Visa is the brand on a ton of cards, it’s not actually a bank or credit issuer. Banking partners such as Bank of America or JPMorgan Chase are the ones taking credit risk. Visa makes money by taking a cut of every transaction spent on its network, which it then splits up and shares with its banking partners.

Visa’s business is effectively a take rate on global economic growth. First, as global consumer spending grows, Visa’s payment volume grows. Second, Visa benefits from the global transition of cash payments to cashless digital transactions. These are two simple tailwinds that have been in place for multiple decades and should continue in the coming decades as well.

Steady growth, inflation protection

If you look at Visa’s financials over time, revenue keeps moving up and to the right. Excluding the pandemic period, when global spending ground to a halt, Visa’s trailing-12-month revenue has grown at a steady clip for the last 10 years. Ten years ago, revenue was a tad over $12 billion. Over the past 12 months, it was $35 billion. I would expect this steady growth to continue over the next 10 years as well.

Operating profit has been even better. Visa has minimal variable costs on its network, meaning it earns high incremental profit margins when revenue grows. This leads to bottom-line profit margin expansion. Operating margin is now 67%, highlighting how amazing Visa’s business model is. This margin should expand slightly over the next 10 years with incremental margins well over 90% on new payment-volume flows.

Don’t forget inflation protection. Since Visa’s revenue comes as a percent of payment volume on its network, it is one of the few businesses that benefits from inflation. Higher prices mean more money coming to Visa as an inherent inflation edge. It really is one of the best business models in the world. This is why payment volume grew from $10.4 trillion in 2021 to $12.3 trillion in 2023.

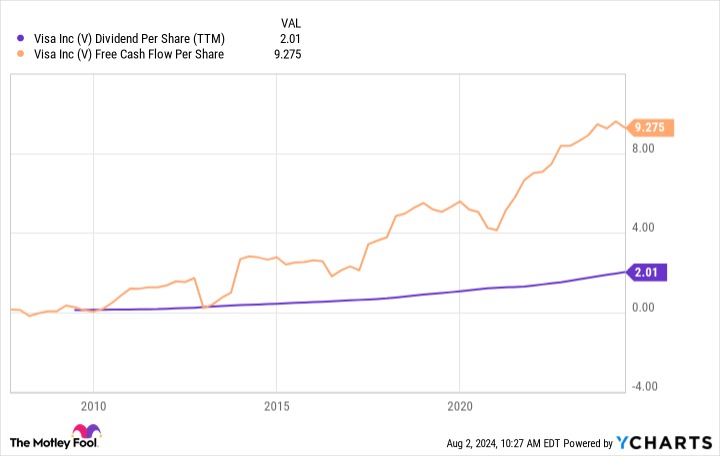

V Dividend Per Share (TTM) data by YCharts.

Why the dividend can keep growing

Okay, that is enough about the business model. What about the recent numbers? Last quarter, Visa’s payment volume grew 7% year over year. However, due to faster growth from higher-margin cross-border volume and the growth of its analytics business, Visa’s revenue grew 10% in the quarter to $8.9 billion. Net income grew 17% to $4.9 billion.

Over the long haul, I expect Visa’s payment volume to grow at 5% to 10% annually from a combination of economic growth, inflation, and the transition to digital payments. Add in margin expansion and new revenue lines, and I think earnings can grow at over 10% per year.

This will mean tons of cash flow accumulating on Visa’s balance sheet that it can return to shareholders in the form of dividends. At Tuesday’s prices, Visa has a dividend yield of only 0.80%, but don’t let that dissuade you. The dividend per share has grown by a whopping 1,800% since being instituted in 2009. At $2.01 over the last 12 months, the dividend per share is well below the $9.30 of free cash flow per share Visa generates.

A huge separation of free cash flow per share and dividend per share means that Visa has room to grow its dividend by 4 times even if its free cash flow per share doesn’t grow. I still think it will grow by a large amount due to the revenue and earnings drivers highlighted above. Plus, management is now aggressively repurchasing stock. Shares outstanding have fallen by 11% in the last five years. Fewer shares outstanding mean more room to raise the dividend per share, all else being equal. It helps add some juice to free-cash-flow per-share growth.

Add everything together, and I believe Visa is the ultimate dividend-growth stock. Buy the dip on the dominant payments giant and watch the dividends pile up in your brokerage account over the next few decades.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

-

Amazon: if you invested $1,000 when we doubled down in 2010, you’d have $18,135!*

-

Apple: if you invested $1,000 when we doubled down in 2008, you’d have $39,543!*

-

Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $322,793!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of August 6, 2024

Brett Schafer has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Visa. The Motley Fool has a disclosure policy.

Want to Get Rich? Buy the Dip on This Dividend-Growth Stock and Never Sell was originally published by The Motley Fool