These 2 “Strong Buy” Penny Stocks Are Poised for a Big Rally, Say Analysts

Investors are constantly on the hunt for stocks that offer solid returns. However, finding these stocks can be challenging and sometimes expensive. Shares of well-known companies like Apple and Microsoft can cost hundreds of dollars for just a single share. However, there are opportunities to invest in stocks with strong growth potential without spending a fortune.

Penny stocks, which are priced under $5 per share, present an interesting mix of potential rewards and risks. Due to their low prices, even small price increases can lead to substantial percentage gains on the investment.

Although penny stocks can deliver massive returns, there could be a reason they are changing hands at such low levels. These names may face significant challenges, such as overwhelming headwinds or poor fundamentals.

The bottom line? Doing some research is necessary before pulling the trigger on any penny stock.

Fortunately, the Street’s analysts are willing to do the digging for you, and their expertise helps identify stocks likely to experience significant gains.

With this in mind, we’ve used the TipRanks database to pinpoint a couple of penny stocks that the analysts believe are poised for a big rally. According to the data, each stock has a Strong Buy consensus rating from the Street and boasts triple-digit upside potential. Let’s take a closer look.

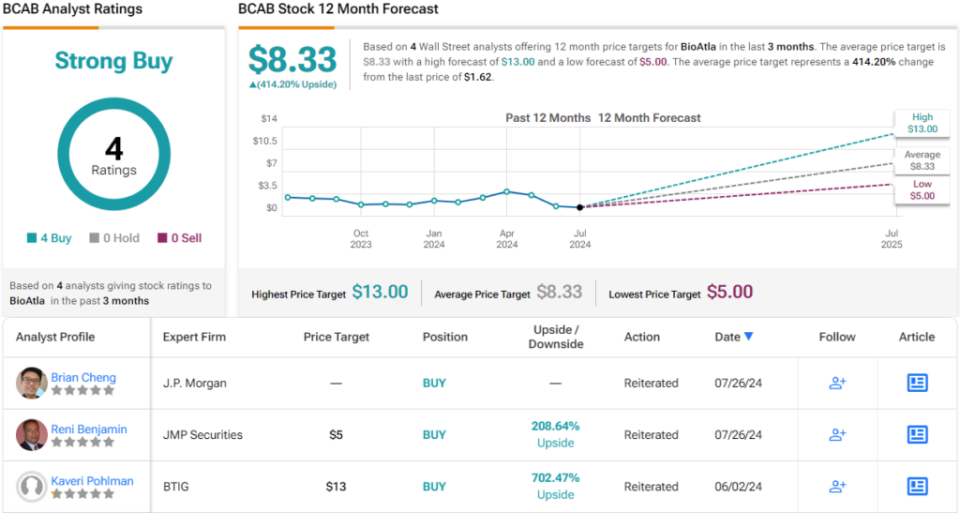

BioAtla (BCAB)

The first penny stock analysts are betting on is BioAtla, a micro-cap biopharma company dedicated to developing innovative cancer treatments. The company focuses on creating a novel class of antibody-based therapeutic agents targeting solid tumor cancers. To this end, BioAtla has introduced a line of conditionally active biologics (CABs) into the clinical research pipeline. These CABs enable the development of drug candidates that directly target known tumor antigens – elements that have previously proven resistant to existing drug treatments.

BioAtla’s approach first identifies the necessary target to destroy the cancer cell, then identifies the needed potency of the drug candidate, and finally reduces the off-tumor toxicity of the therapeutic agent. The company describes these as the ‘fundamental challenges’ of cancer treatment, and has chosen to meet them head-on. BioAtla’s goal is to create novel cancer drugs that will offer curative potential or extended survival, for an improved quality of life.

The leading candidate in BioAtla’s pipeline is mecbotamab vedotin, also known as BA3011. This CAB antibody-drug conjugate (ADC) targets the receptor tyrosine kinase AXL and is being tested in clinical trials for several solid tumor cancers, including undifferentiated pleomorphic sarcoma (UPS) and non-small cell lung cancer (NSCLC). The UPS trial, which has enrolled 20 patients, is a potentially registrational Phase 2 study. The company plans to present multiple patient scans to the FDA in the second half of 2024 to discuss the progress and future direction of the study. Additionally, Phase 2 studies have shown clinical benefits for NSCLC patients with mutant KRAS (mKRAS) variants.

BioAtla’s second clinical candidate is ozuriftamab vedotin, also called BA3021. This is another CAB ADC that directly targets ROR2. This is a transmembrane receptor tyrosine kinase found in multiple solid tumors and is notable in head and neck cancers, lung cancers, and melanoma. When overexpressed, ROR2 is frequently associated with poor prognosis and resistance to existing cancer treatments. Ozuriftamab vedotin has shown promise in a Phase 2 trial against squamous cell carcinoma of the head and neck (SCCHN), and on July 23, the company announced that the drug candidate had received the FDA’s Fast Track designation for that indication.

Additionally, BioAtla is developing evalstotug (BA3071), a conditionally activated anti-CTLA4 monoclonal antibody. Evalstotug has demonstrated anti-tumor activity in heavily pretreated patients across various solid tumors. Currently, BioAtla is enrolling patients in a Phase 2 study evaluating evalstotug in combination with pembrolizumab for first-line melanoma and with pembrolizumab plus chemotherapy for first-line NSCLC. Moreover, BioAtla plans to initiate a Phase 3 study for first-line BRAF mutated melanoma by the end of 2024.

Given the potential of BioAtla’s drug candidates and its current share price of $1.62, JMP analyst Reni Benjamin believes that this is an opportune time to invest in the company.

“With four distinct assets in clinic, encouraging data in KRAS mutant NSCLC, potential for a partnership in 2H24, and a cash position of $62.1MM (pro forma), we continue to view shares as undervalued, especially given the recent weakness,” Benjamin noted. “During the 2024 ESMO Congress [September 13 to 17, 2024], we expect data from the Phase 2 study evaluating BA3021 in patients with recurrent or metastatic (r/m) head and neck squamous cell carcinoma (HNSCC).”

To this end, Benjamin rates BCAB a Buy, and his $5 price target suggests the stock will gain a solid 208% in the year ahead. (To watch Benjamin’s track record, click here)

The broader Wall Street consensus is even more optimistic. BCAB holds a Strong Buy consensus rating, based on 4 unanimous Buy recommendations, with an average price target of $8.33, implying a potential upside of 414% from the current share price. (See BCAB stock forecast)

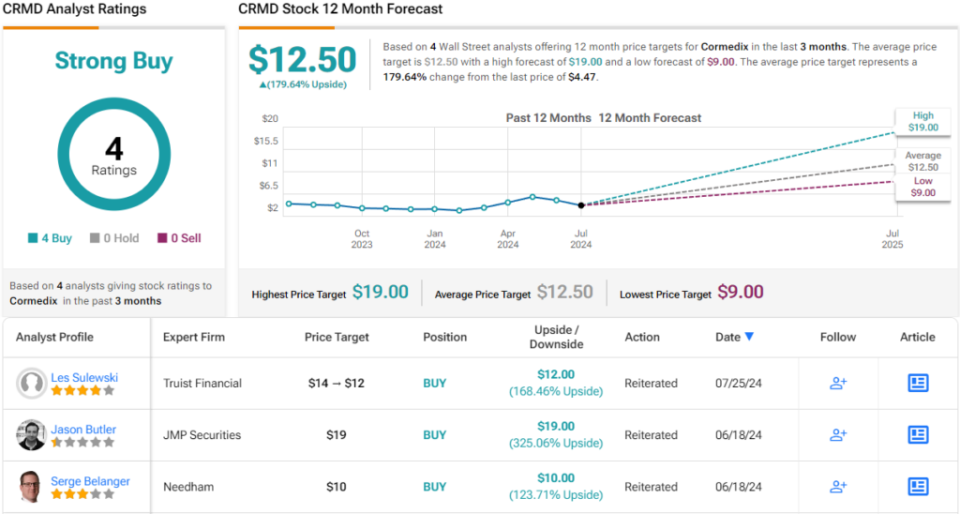

CorMedix (CRMD)

Next up is CorMedix, a biopharma company working to develop new treatments for infectious and/or inflammatory diseases. Specifically, this company is targeting infection due to intravenous catheterization. This is a common medical intervention, used in a wide range of medical procedures; IVs are used to administer drug therapies, to provide hydration and nutrition, and are necessary in such life-saving treatments as kidney dialysis. The use of IV catheters, however, also provides a site for potential infection, as bacteria can invade the patient through the needle site. CorMedix is aiming to prevent, reduce, or treat these infections, to head off serious complications.

CorMedix has developed a new product, dubbed DefenCath, which makes use of two medications. The primary component, taurolidine, is a synthetic broad-spectrum antimicrobial and antifungal agent with anti-inflammatory properties, making it ideal for preventing catheter infections. Paired with the anticoagulant heparin, DefenCath is used as a catheter lock solution to prevent bloodstream infections related to catheter use.

DefenCath was approved for use by the FDA in November of last year, and CorMedix has been working to commercialize the product for in-patient use. In addition, the company has recently announced several updates that bode well for the eventual adoption of DefenCath in regular use. In May of this year, the company announced an agreement with a top-tier dialysis provider, which will make DefenCath available in 500 dialysis facilities across the US. This was followed in July by CorMedix’s announcement that it had begun the commercial launch of DefenCath in outpatient dialysis facilities, with outpatient reimbursement authorized by the Center for Medicare and Medicaid Services. In addition, in June, CorMedix received ‘supportive feedback’ from the FDA on a potential label expansion for DefenCath.

All of this points to increasing adoption of this product, and that has caught the attention of analyst Les Sulewski, who covers CorMedix for Truist.

“We remain buyers of the stock as we think Defencath should become the standard of care across all dialysis procedures. Inpatient is progressing as expected with CRMD planning to contact over 900 hospitals responsible for over 65% of inpatient dialysis procedures. Outpatient is more of an unknown, but we remain encouraged with recent signings and the potential for contracts with bigger providers. Potential label expansion in pediatrics, TPN and Oncology are all plausible and offer upside to TAM,” Sulewski opined.

These comments back up Sulewski’s Buy rating on this stock, while his $12 price target indicates his confidence in a 168% share appreciation for the next 12 months. (To watch Sulewski’s track record, click here)

Overall, CRMD’s Strong Buy consensus rating is based on 4 unanimously positive analyst reviews, and the $4.47 share price and $12.50 average target price together suggest that the stock has a one-year upside of ~180%. (See CRMD stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.