There’s a 12% correction looming for the stock market by the end of the year, Stifel says

-

Stifel warns of a sharp stock market correction by year-end, with the S&P 500 potentially dropping 12%.

-

Chief equity strategist Barry Bannister said high valuations and speculative investor behavior are a concern.

-

“Our instruments tell us to expect an S&P 500 correction to the very low 5,000s by 4Q24,” Bannister said.

Investors should prepare for a sharp and quick correction in the stock market before the end of the year, according to Stifel.

In a note on Thursday, chief equity strategist Barry Bannister of Stifel warned that the S&P 500 could trade 12% lower in the fourth quarter.

“Our instruments tell us to expect an S&P 500 correction to the very low 5,000s by 4Q24,” Bannister said.

According to Bannister, there are a number of factors that are giving him cause for concern, including the idea that investors are exhibiting the type of behavior that is present during bubbles and manias.

“Just as countries that go rogue become almost un-investable, investors caught in the grips of a speculative fever become almost un-analyzable,” Bannister said.

For one, Bannister is concerned about current stock market valuations, which are approaching a “near three-generation high” based on the S&P 500’s price-to-earnings multiple of around 24x.

In addition, the sharp outperformance of large-cap growth stocks relative to value stocks is approaching the same peak seen in February 2000 and August 2020, which both served as a warning of an imminent bear market.

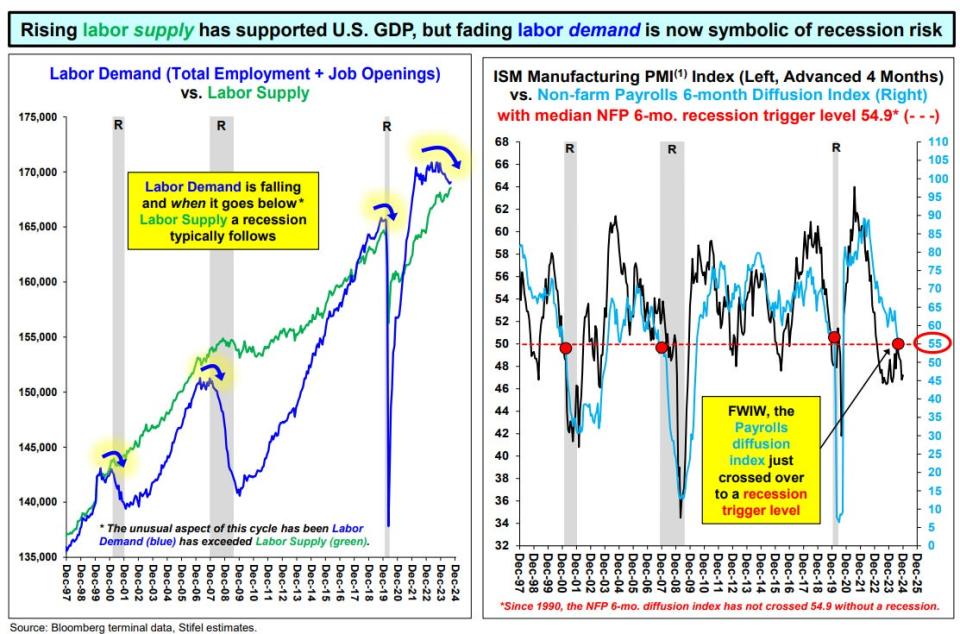

On the labor front, while Bannister admits that rising labor supply via increased immigration has supported economic growth, with US GDP growing at a rate above pre-pandemic trend levels, overall labor demand has been fading.

“Fading labor demand is now symbolic of recession risk,” Bannister said.

Bannister highlighted that the non-farm payroll 6-month diffusion index just crossed below a “recession trigger level.”

The diffusion index helps measure the breadth of job gains or losses across all economic industries.

Shifting to the election in November, Bannister said the typical “pre-election juice” for the economy is likely to fade towards the end of the year, as election promises from both sides of the aisle retreat and reality sets in that it’s hard to pass significant legislation in what could be a divided government.

“Pre-election juice for the economy may recede at year-end, causing stocks (which anticipate the future) to dip ~4 months in advance, and that is 4Q24E,” Bannister explained.

Finally, Bannister said that many investors are not appreciating the risks of a bubble in technology stocks, akin to what happened during the dot-com craze nearly 25 years ago.

“It takes one generation to forget the dangers of a bubble, and it is Groundhog Day versus the 1990s Tech Bubble; in reality ‘new tech’ isn’t even ‘new’ and today’s low Equity Risk Premium appears to us to lock-in a weak S&P 500 next-10-year compound annual real total return close to 3% real and 6% nominal,” Bannister said.

Read the original article on Business Insider