Stocks Rally as Nvidia Up 11% After Bullish Call: Markets Wrap

(Bloomberg) — Stocks staged a powerful rebound amid a rally in beaten-down chipmakers, with the latest economic data bolstering bets the Federal Reserve will signal a rate cut in September.

Most Read from Bloomberg

Following a selloff that put the Nasdaq 100 on the brink of a correction, the gauge climbed 3%. Nvidia Corp. surged 12% after being renamed the top US chip pick by Morgan Stanley analysts. Advanced Micro Devices Inc. jumped on a bullish outlook. As Meta Platforms Inc. gets ready to report earnings, investors hope it can do a better job than Microsoft Corp. and Alphabet Inc. in convincing Wall Street that lofty spending on AI will pay off.

It’s Fed day — which looms over a busy period for earnings and a heavy newsflow that just won’t let up. The central bank isn’t expected to lower rates Wednesday, despite calls from some former policymakers. Even if officials generally believe rates should be lower, they could spook the market by moving suddenly. If they wait, they need to have a clear reason why.

“If you say you’re waiting until the next meeting because you want to see some data between now and the next meeting, that makes markets wonder ‘OK, well, what is it that could derail a rate cut between now and the next meeting?’,” Former St. Louis Fed President James Bullard told Bloomberg Television. “If you do react to that data, that’s kind of data-point dependent.”

To Thierry Wizman at Macquarie, the Fed will need to “thread a needle.”

“A too-strong signal of a coming September rate cut may scare traders into thinking that the Fed sees abrupt economic weakness ahead,” he noted. “A too-weak signal, where a rate cut hinges on the data ‘evolving as we expect’ in the context of lingering attentiveness to inflation may not sound satisfactory to the bulls.”

The S&P 500 climbed 1.6%. A Bloomberg gauge of the “Magnificent Seven” megacaps jumped 3%. The $22 billion VanEck Semiconductor exchange-traded fund (ticker: SMH) climbed 6%. The Russell 2000 of small firms added 1%. Mastercard Inc. surged on a profit beat. Boeing Co. gained after appointing a new chief. Humana Inc. tumbled after warning on higher hospital admissions.

Treasury 10-year yields declined four basis points to 4.10%. The US Treasury left its quarterly issuance of longer-term debt unchanged for the second straight time, and maintained its guidance that it doesn’t expect to need increasing issuance of notes and bonds for “several quarters.”

The Bloomberg Dollar Spot Index fell 0.5%. Oil jumped after Hamas said Israel killed its political leader, stoking geopolitical risks. The yen rallied as the Bank of Japan raised interest rates and announced plans to cut bond purchases.

“We expect the Fed to lean dovish today,” said Fawad Razaqzada at City Index and Forex.com. “Recent comments from Fed officials, coupled with lackluster US economic data, highlight the need for a less restrictive monetary policy.”

Fed officials are likely to move closer to lowering rates from a two-decade high by signaling a potential rate cut in September, though they may stop short of providing details beyond that. The decision will be announced via a post-meeting statement at 2 p.m. in Washington. Jerome Powell will hold a press conference 30 minutes later.

Powell’s press conference is the usual “wild card,” according to Win Thin and Elias Haddad at Brown Brothers Harriman & Co.

“While risks are skewed that Powell leans dovish, we do not expect him to validate the aggressive easing that’s priced in by the markets,” they noted.

A survey conducted by 22V Research shows 75% of investors believe that officials will first cut because of a soft landing and that inflation is on a Fed-friendly path toward sub-3%. So there will be a cut because policy doesn’t need to be as restrictive.

“This is 11% higher than when we asked last month. Investor confidence around a soft-landing is increasing,” said Dennis DeBusschere, founder of 22V.

In addition, 44% of the investors polled by 22V expect the Fed meeting/presser to be “mixed/negligible,” 38% believe “risk-on” and 18% “risk-off.”

In economic news, a broad gauge of US labor cost growth closely watched by the Fed cooled in the second quarter by more than forecast. American companies added the fewest number of workers since the start of the year and wage growth slowed. Separately, pending home sales rose for the first time in three months.

“The Fed could justify a rate cut today based on current data on the job market and inflation, as well as the plausible case for both to cool in the near term,” said Bill Adams at Comerica Bank. “But the Fed is also concerned about their credibility, which they fear may have been dented by inflation’s overshoot in the last three years.”

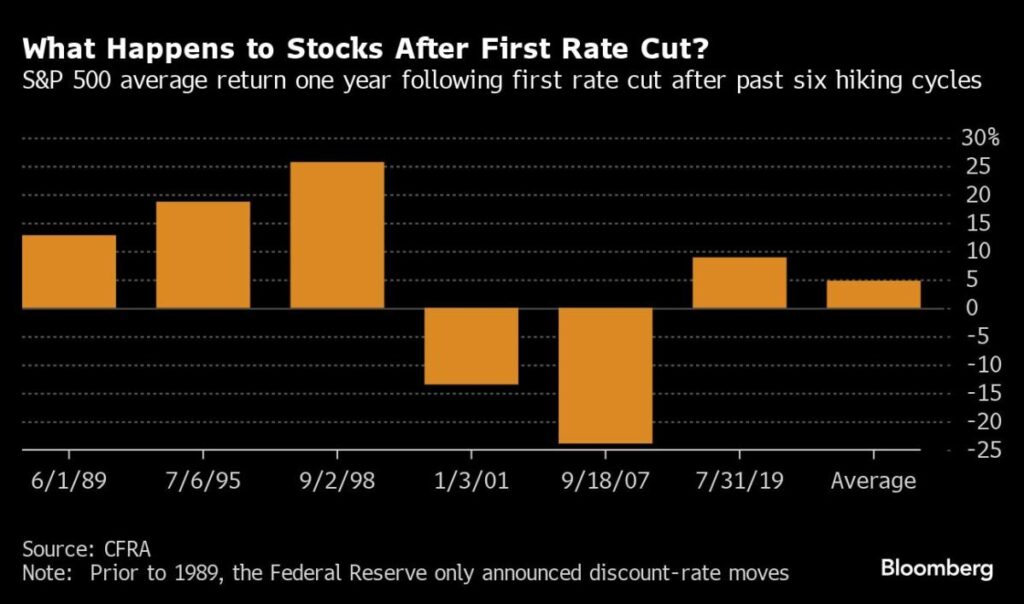

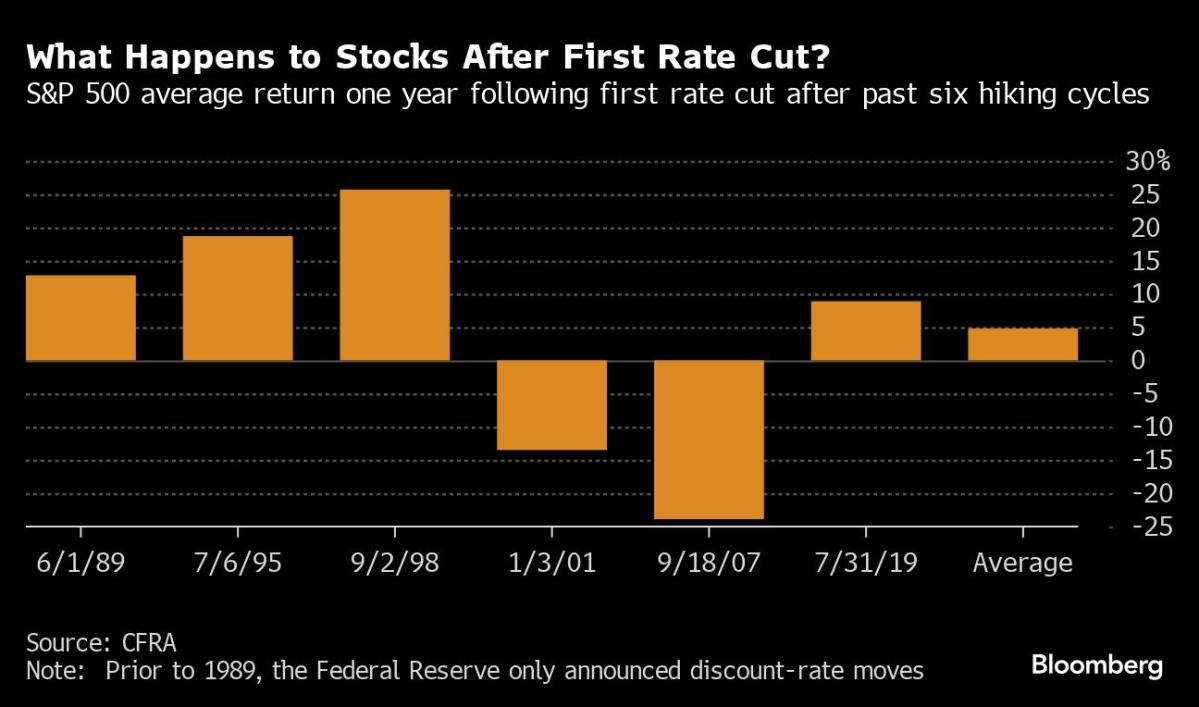

The road ahead for investors is looking rough right now as policy gatherings by the world’s most important central banks come at the start of what’s historically the worst two months for US stock returns.

In the past three decades, the S&P 500 in August and September has averaged respective losses of 0.5% and 0.7%, data compiled by Bloomberg show. Those seasonal patterns create another headache for traders since the broadening of this year’s powerful stock-market rally hangs on what the Fed signals about interest rates once its two-day meeting wraps up this afternoon.

“We continue to see a favorable backdrop for US equities and advise investors to maintain a full allocation to the US market,” said Solita Marcelli at UBS Global Wealth Management. “We believe AI beneficiaries should continue to account for a substantial part of portfolios as the technology drives further growth in the years ahead, but we also see opportunities in other quality companies, including those exposed to secular trends like the energy transition, blue economy, and water scarcity.”

Corporate Highlights:

-

The Biden administration is preparing to implement a sweeping new trade restriction — known as the foreign direct product rule — to keep China from accessing advanced semiconductor technology. But Tokyo Electron Ltd., ASML Holding NV and other chip companies in the Netherlands and Japan are expected to be exempt from the new limits, said the people, asking not to be identified discussing private negotiations.

-

Intel Corp. plans to eliminate thousands of jobs to reduce costs and fund an ambitious effort to rebound from an earnings slump and market share losses.

-

Starbucks Corp. delivered results that were in line with expectations, assuaging investors who had been bracing for another meltdown after being blindsided by the previous quarter’s slump.

-

Pinterest Inc. warned that revenue in the current quarter will be lower than analysts’ predictions.

-

Delta Air Lines Inc. is bracing for a $500 million negative impact from the technology breakdown this month that led to thousands of canceled flights and tarnished the carrier’s reputation.

-

T-Mobile US Inc. reported new monthly mobile-phone subscribers that exceeded analyst estimates, joining its peers in wooing new customers in the second quarter.

-

Dupont de Nemours Inc. second-quarter profit exceeded investor expectations, as AI-driven demand for semiconductors drove gains in its electronics business.

-

Match Group Inc. announced plans to cut 6% of its staff and delivered better-than-expected earnings.

Key events this week:

-

Eurozone S&P Global Eurozone Manufacturing PMI, unemployment, Thursday

-

US initial jobless claims, ISM Manufacturing, Thursday

-

Amazon, Apple earnings, Thursday

-

Bank of England rate decision, Thursday

-

US employment, factory orders, Friday

Some of the main moves in markets:

Stocks

-

The S&P 500 rose 1.6% as of 1:06 p.m. New York time

-

The Nasdaq 100 rose 2.7%

-

The Dow Jones Industrial Average rose 0.7%

-

The MSCI World Index rose 1.6%

-

Bloomberg Magnificent 7 Total Return Index rose 3.1%

-

The Russell 2000 Index rose 1.1%

Currencies

-

The Bloomberg Dollar Spot Index fell 0.4%

-

The euro was little changed at $1.0810

-

The British pound was little changed at $1.2838

-

The Japanese yen rose 1.4% to 150.62 per dollar

Cryptocurrencies

-

Bitcoin rose 0.4% to $66,443.13

-

Ether rose 0.4% to $3,294.77

Bonds

-

The yield on 10-year Treasuries declined four basis points to 4.10%

-

Germany’s 10-year yield declined four basis points to 2.30%

-

Britain’s 10-year yield declined seven basis points to 3.97%

Commodities

-

West Texas Intermediate crude rose 4.1% to $77.77 a barrel

-

Spot gold rose 0.6% to $2,426.15 an ounce

This story was produced with the assistance of Bloomberg Automation.

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.