Stock Meltdown Puts S&P 500 on Brink of Correction: Markets Wrap

(Bloomberg) — A renewed bout of volatility hit global markets as recent talk about a US economic recession — mostly seen as premature — spurred warnings that this year’s sizzling stock rally has gone too far.

Most Read from Bloomberg

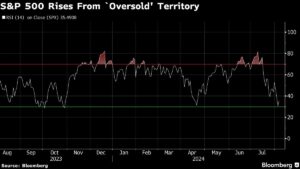

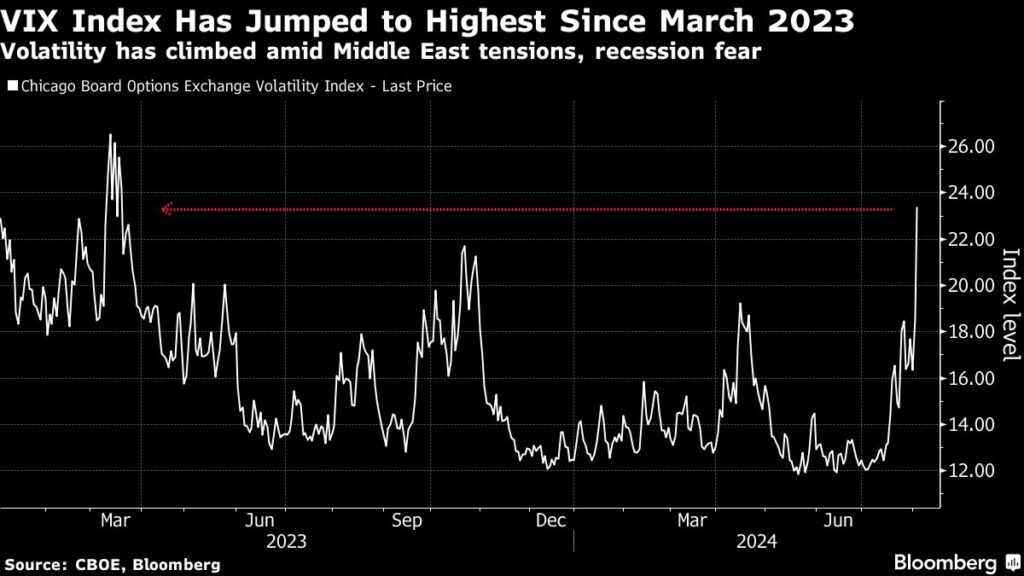

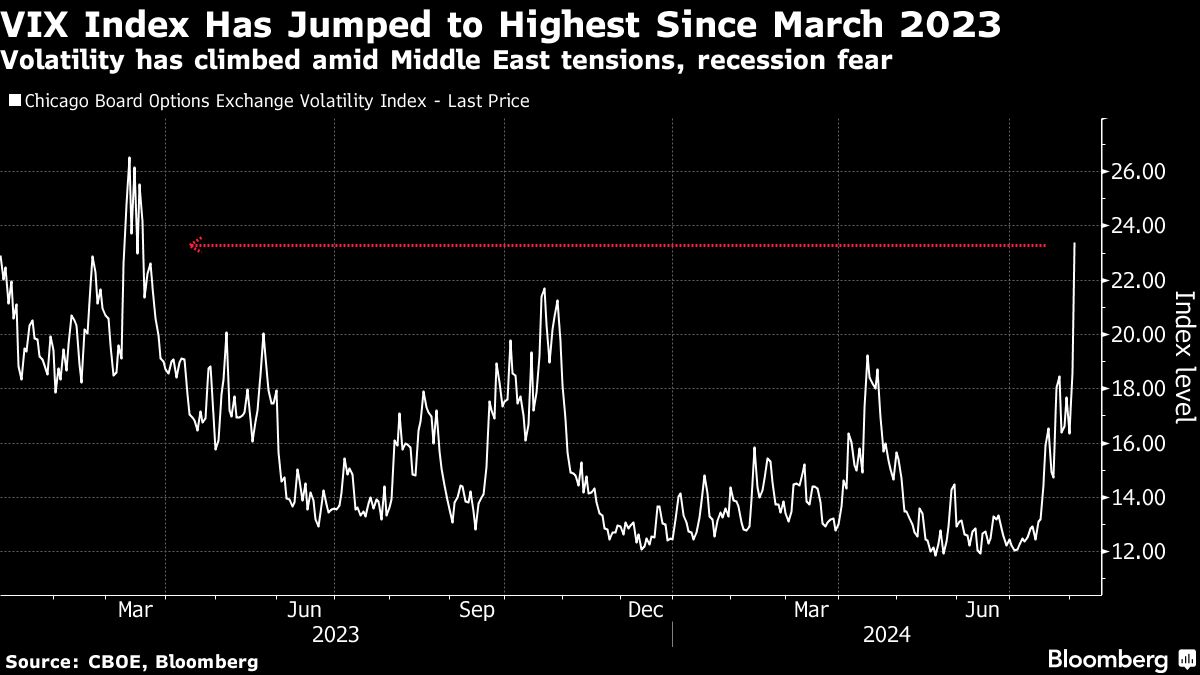

From New York to London and Tokyo, equities got pummeled. Just as markets started celebrating signals from the Federal Reserve about a first rate cut, they were hit by a perfect storm — weak economic data, underwhelming corporate earnings, stretched positioning and poor seasonal trends. While the S&P 500 pared some of its losses, it suffered the biggest plunge in about two years amid strong trading volume. The tech-heavy Nasdaq 100 saw its worst start to a month since 2008. Wall Street’s “fear gauge” – the VIX – at one point registered its largest spike in data going back to 1990.

Treasuries lost some steam after a surge that briefly drove two-year yields — which are sensitive to monetary policy — below those on 10-year bonds. Traders are betting the economy is on the verge of deteriorating so quickly the Fed would need to start easing policy aggressively. The repricing was so sharp that the swap market earlier assigned a 60% chance of an emergency rate reduction by the Fed over the coming week. Those odds subsequently ebbed.

“The economy is not in crisis, at least not yet,” said Callie Cox at Ritholtz Wealth Management. “But it’s fair to say we’re in the danger zone. The Fed is in danger of losing the plot here if they don’t better acknowledge cracks in the job market. Nothing is broken yet, but it’s breaking and the Fed risks slipping behind the curve.”

At LPL Financial, Quincy Krosby said that after such a strong rally, valuations, sentiment and positioning had become stretched.

“What markets are experiencing is an unwinding of that bullish positioning,” she said. “Watch for signs of a capitulating Fed, timely evidence of a growing economy, and a successful test of the 200-day moving average on the S&P 500 for signs a bottom may be in.”

The S&P 500 lost 3%, extending a tumble from its peak to 8.5%. US 10-year yields were little changed at 3.78%. The dollar fell. A gauge of perceived risk in the US corporate credit markets soared, with the turmoil effectively shutting down bond sales on what had been expected to be among the busiest days of the year. Bitcoin sank about 10%.

Subscribe to the Bloomberg Daybreak podcast on Apple, Spotify or anywhere you listen.

The wave of selling hit a fever pitch in Japan as traders rushed to unwind popular carry trades, powering a 2% jump in the yen and causing the Topix stock index to shed 12% and close the day with the biggest three-day drop in data stretching back to 1959. The rout wiped out $15 billion of SoftBank Group Corp.’s value on Monday.

“The market is a tug of war between fear and greed,” said Nancy Tengler at Laffer Tengler Investments. “In my 40+ years as a professional investor, it has always paid to buy when others are fearful. Volatility is the friend of long-term investors.”

The US stock plunge is vindicating some prominent bears, who are doubling down with warnings about risks from an economic slowdown. JPMorgan Chase & Co.’s Mislav Matejka said equities are set to stay under pressure from weaker business activity, a drop in bond yields and a deteriorating earnings outlook. Morgan Stanley’s Michael Wilson warned of “unfavorable” risk-reward.

“This doesn’t look like a ‘recovery’ backdrop that was hoped for,” Matejka wrote. “We stay cautious on equities, expecting the phase of ‘bad is bad’ to arrive,” he added.

Market veteran Ed Yardeni said that the current equity selloff bears some similarity to the 1987 crash, when the economy averted a downturn despite investor fears at the time.

“This is very reminiscent, so far, of 1987,” Yardeni said on Bloomberg Television. “We had a crash in the stock market — that basically all occurred in one day — and the implication was that we were in, or about to fall into, recession. And that didn’t happen at all. It had really more to do with the internals of the market.”

To Seema Shah at Principal Asset Management, economic weakness concerns will likely prove overdone, but the depth of the negative narrative now implies that an imminent market turnaround is unlikely. A sustained market recovery needs a catalyst, or likely a combination of catalysts, including stabilization of the Japanese yen, strong earnings numbers, and solid data releases.

“It’s complicated — return of the ‘R’ word derailing the Goldilocks trade,” said Maxwell Grinacoff at UBS Investment Bank. “Similar to what we witnessed amidst the small-cap rotation a few weeks ago, the degree of moves was clearly exacerbated by stretched positioning. The difference today is there is fundamental backing to elevated levels of risk premia, from both a macro and earnings perspective.”

After a very strong first half, the market had become extended on a short-term basis and the bar for positive surprises too high — and a little bit of bad news has gone a long way, according to Keith Lerner at Truist Advisory Services.

“From a stock market perspective, our base case has not changed,” Lerner said. “Our work still suggests the bull market deserves the benefit of the doubt. However, we have been expecting a choppier environment into the back half of July and August given the sharp rebound from April, stretched sentiment, and the fact that we’re entering a seasonally weaker period of the calendar year.”

Moreover, after strong first halves, historically we have seen a typical pullback of 9% at some point, even while markets still tended to end higher by the end of the year.

Notably, over the past 40 years, the S&P 500 has averaged a maximum intra-year pullback of 14%. Despite this, stocks have still shown an average return (not compounded) of 13% and risen in 33 out of 40 of those years, or 83% of the time, Lerner said.

“While always uncomfortable and typically accompanied by bad news, pullbacks are the admission price to the stock market,” Lerner said. “This is what provides the potential for higher longer-term returns relative to most other asset classes.”

Investors should rationally consider the current landscape, according to Russell Price at Ameriprise. Are markets correcting because they may have seen equity market gains come too far too fast? Or are markets falling because of true threats over economic conditions and the possibility of a global recession?

“We believe, the preponderance of evidence supports the former,” Price says. “The US economy is currently moderating to more sustainable rates, but a near-term recession is not the most likely path ahead, in our view. Even if it were, we believe central banks have ample fire power to lower rates to restimulate activity, if necessary, which should once again entice capital toward stocks.”

When investors turned their calendars to August, they may have flipped the narrative on the economy at the same time, according to John Lynch at Comerica Wealth Management.

“It’s been less than two weeks since the second quarter GDP report surprised to the upside, with equity markets hovering near record levels, yet there is growing sentiment is that the Fed has waited too long to cut interest rates and is now behind the curve,” Lynch said. “While we’re not completely sold on the new narrative, the one thing that seems certain is that there is more volatility ahead.”

Investors should hedge their risk exposure even if they own high quality assets as US stocks extend losses, according to Goldman Sachs Group Inc.’s Tony Pasquariello.

“There are times to go for the gas, and there are times to go for the brake — I’m inclined to ratchet down exposures and roll strikes,” Pasquariello wrote. He added that it’s difficult to think that August will be one of those months where investors should carry a significant portfolio risk.

Systematic funds have offloaded more than $130 billion of global stock bets in recent weeks. Now these rules-based players threaten to take their selling to a whole new level as volatility spikes.

Strategies including risk parity, vol-targeting and trend following will dispose $70 billion to $80 billion of shares Monday, with at least $90 billion more to unwind over the next four sessions, according to estimates from Morgan Stanley’s trading team.

To Michael Gapen at Bank of America Corp., markets are getting ahead of the Fed again.

“Incoming data have raised concerns that the US economy has hit an ‘air pocket.’ A rate cut in September is now a virtual lock, but we do not think the economy needs aggressive, recession-sized cuts.”

Equity markets experienced one of the most severe rotations in years in July, with small cap and value stocks surging and mega cap tech stocks selling off. A key question for investors is whether this move continues or fades out similar to previous rotations, according to Jeff Schulze at ClearBridge Investments.

“While a growth scare could spark a retracement of this rotation, we ultimately expect a pickup in economic growth which should favor small cap, value and cyclicals,” he said. “Leadership rarely moves in a straight line, and we believe the near term (the next several months) could see an oscillation that favors the previous leadership on the perception of safety if the economy cools further. Ultimately, we believe a soft landing will play out.”

As the selloff in global stocks intensified Monday, JPMorgan Chase & Co.’s trading desk said the rotation out of the technology sector might be “mostly done” and the market is “getting close” to a tactical opportunity to buy the dip.

Buying of stocks by retail investors has slowed quickly, positioning by trend-following commodity trading advisers has fallen a lot across equity regions and hedge funds have been net sellers of US stocks, JPMorgan’s positioning intelligence team wrote in a Monday note to clients.

“Overall, we think we’re getting close to a tactical opportunity to buy-the-dip,” wrote John Schlegel, JPMorgan’s head of positioning intelligence. “That said, whether we get a strong bounce or not could depend on future macro data.”

“The euphoria of the first quarter is quickly becoming a distant memory as weaker economic data is raising voices for a Fed cut in rates soon, and maybe before their next meeting,” said Paul Nolte at Murphy & Sylvest Wealth Management. “We are in the early stages of the ‘dog days of summer’ and things are heating up on Wall Street.”

Corporate Highlights:

-

Palantir Technologies Inc. raised its annual outlook, citing continuing demand for its artificial-intelligence software.

-

A federal judge on Monday ruled that Google has illegally monopolized the search market, hading the government an epic win in its first major antitrust case against a tech giant in more than two decades.

-

Nvidia Corp.’s upcoming artificial intelligence chips will be delayed due to design flaws, The Information reported, citing two unidentified people who help produce the chip and its server hardware.

-

Dell Technologies Inc. is cutting jobs as part of a reorganization of its sales teams that includes a new group focused on artificial intelligence products and services.

-

Tyson Foods Inc. shares surged, bucking a broad retreat in equity markets, as quarterly earnings beat the highest of analyst estimates on a rebound in chicken profits.

Key events this week:

-

Australia rate decision, Tuesday

-

Eurozone retail sales, Tuesday

-

China trade, forex reserves, Wednesday

-

US consumer credit, Wednesday

-

Germany industrial production, Thursday

-

US initial jobless claims, Thursday

-

Fed’s Thomas Barkin speaks, Thursday

-

China PPI, CPI, Friday

Some of the main moves in markets:

Stocks

-

The S&P 500 fell 3% as of 4 p.m. New York time

-

The Nasdaq 100 fell 3%

-

The Dow Jones Industrial Average fell 2.6%

-

The MSCI World Index fell 3.1%

-

Bloomberg Magnificent 7 Total Return Index fell 4.3%

-

The Russell 2000 Index fell 3.3%

Currencies

-

The Bloomberg Dollar Spot Index fell 0.3%

-

The euro rose 0.4% to $1.0960

-

The British pound fell 0.2% to $1.2777

-

The Japanese yen rose 1.8% to 143.85 per dollar

Cryptocurrencies

-

Bitcoin fell 9.3% to $53,654.63

-

Ether fell 12% to $2,415.61

Bonds

-

The yield on 10-year Treasuries was little changed at 3.78%

-

Germany’s 10-year yield advanced two basis points to 2.19%

-

Britain’s 10-year yield advanced four basis points to 3.87%

Commodities

-

West Texas Intermediate crude rose 0.3% to $73.76 a barrel

-

Spot gold fell 1.4% to $2,408.16 an ounce

This story was produced with the assistance of Bloomberg Automation.

–With assistance from Robert Brand, Lynn Thomasson and Lu Wang.

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.