Intel Stock Is Cheaper Than Its Ever Been

Intel‘s (NASDAQ: INTC) turnaround was always going to be a drawn-out affair. The company has been making massive investments in manufacturing to catch up to and surpass TSMC in terms of manufacturing technology. The Intel 18A process, set to be ready by the end of the year and scale up throughout 2025 and 2026, is expected to battle the best process nodes TSMC has to offer.

Intel is aiming to use its new manufacturing processes to revitalize its PC and server-chip businesses, both of which have been held back by delays and missteps on the manufacturing side. The company also has plans to grow into the world’s second-largest foundry by 2030, which would require more than $15 billion in annual external-foundry revenue by the end of the decade. Intel’s goals are ambitious, to say the least.

Not quite according to plan

One downside of Intel’s strategy: It can take years for these manufacturing investments to pay off. The foundry business is currently posting multibillion-dollar losses, the result of heavy spending and essentially no external revenue. Intel has booked at least $15 billion worth of external-foundry business, but much of that won’t be converted into revenue until 2025 or 2026.

As Intel is pouring capital into manufacturing, the company is facing a weak PC market, competitive pressure from AMD, and a priority shift among data-center customers toward AI chips and away from standard CPUs. Intel missed estimates for its second-quarter report earlier this month, and its near-term outlook has become bleak enough to prompt the company to enact a broad cost-cutting plan.

Intel expects to slash its combined operating expenses and capital spending by at least $10 billion in 2025, as well as suspend the dividend to free up cash. This plan includes laying off about 15% of its workforce. Importantly, Intel isn’t pulling back on its manufacturing goals. While the company is reducing its capital spending to a degree, nothing has changed about its long-term foundry targets.

Intel stock tanked on this news. Based on one metric, it’s now cheaper than it’s ever been.

Extreme pessimism

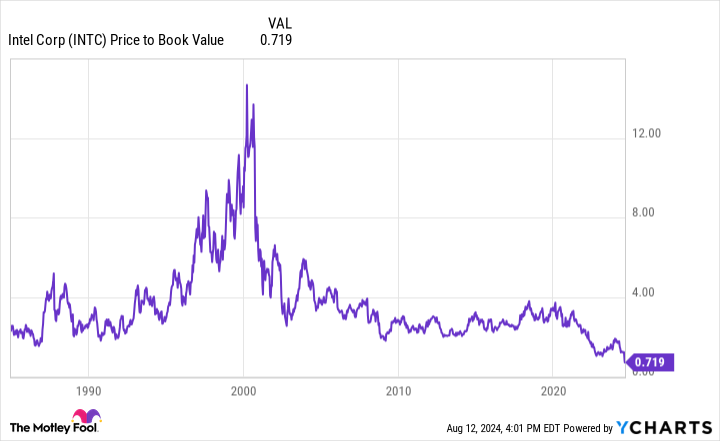

The price-to-book value ratio (P/B), which takes a company’s market capitalization and divides it by assets minus liabilities, is only useful in cases where earnings power is derived from physical assets. A manufacturing company fits the bill, while a software company generally does not.

Intel is very much a manufacturing company. The company had over $100 billion worth of property, plant, and equipment on its balance sheet at the end of Q2, accounting for about half of its total assets. For Intel, the P/B is a useful metric.

Here’s what Intel’s P/B looks like right now:

Here’s the same chart for price-to-tangible bool value, which excludes intangible assets:

You have to go back decades to find a time when Intel was close to this cheap based on these two metrics.

What’s the “correct” P/B ratio for Intel? That’s impossible to answer, but generally speaking, the higher the return on invested capital (ROIC), the higher the P/B ratio should be. A company that manufactures commodities, swinging between profits and losses, shouldn’t trade at much of a premium to book value.

Intel doesn’t make commodities, and it has historically managed a ROIC between 15% and 20%. That metric has tumbled recently as Intel has ramped up investments while facing multiple challenges, but the cost-cutting plan should help the cause.

Intel stock now trades for a bit more than 70% of its book value. The market is assuming that Intel is never going to recover. While the company may never be as dominant in its core markets as it once was, writing it off completely makes little sense.

It’s going to be a tough few years for Intel, but if you think the chance of a turnaround is anything greater than zero, this is a great time to buy the stock.

Should you invest $1,000 in Intel right now?

Before you buy stock in Intel, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Intel wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $668,029!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of August 12, 2024

Timothy Green has positions in Intel. The Motley Fool has positions in and recommends Advanced Micro Devices and Taiwan Semiconductor Manufacturing. The Motley Fool recommends Intel and recommends the following options: long January 2025 $45 calls on Intel and short August 2024 $35 calls on Intel. The Motley Fool has a disclosure policy.

Intel Stock Is Cheaper Than Its Ever Been was originally published by The Motley Fool