Huge News For Philip Morris International Stock: Here’s What Comes Next

The last few years have seen a ton of disruption in the nicotine space. After decades of stable market share from cigarettes, cigars, and chewing tobacco, companies are innovating and changing the sector with new nicotine products that reduce tobacco-related health risks. One company is investing in both sides of the industry: Philip Morris International (NYSE: PM).

The company is the owner of the international Marlboro brand. It has scooped up the leading tobacco-free nicotine pouch brand and is now planning a major capacity expansion in the United States. Here’s what comes next for Philip Morris International, and whether the stock is a buy at current price levels.

Booming nicotine pouch demand

In late 2022, Philip Morris made a big bet in the tobacco-free nicotine pouch space. It made an acquisition of Swedish Match, the owner of the fast-growing Zyn brand with leading market share in the United States, for around $16 billion. Since then, nicotine pouch volume for Zyn has exploded higher.

Last quarter, Zyn volume hit 131.6 million and was growing 40% year over year. For all of 2019, Zyn delivered just 50 million cans in the United States. Volumes are still growing at a healthy double-digit rate, and the company is actually hitting on some supply constraints due to insatiable customer demand.

To match this demand, management just announced a $600 million investment in a new nicotine pouch facility in Colorado that will hit regular production in 2026. Nicotine pouches are still just a small amount of the U.S. market, with analysts expecting double-digit volume growth to continue through 2030. This bodes well for Philip Morris International.

There is even more to be excited about for Philip Morris in nicotine alternatives. Nicotine pouches are expanding to new countries, which can add even more growth to the new segment. The heat-not-burn IQOS brand — which currently has over 30 million customers — will be entering the United States soon. Both these developments could drive tons of growth for Philip Morris International’s new categories, which now make up 39% of total net revenues.

Stable legacy international business

Let’s not forget the profitable legacy cigarette business, which is still generating boatloads of cash flow. Due to Philip Morris International’s exposure to emerging markets, volumes are actually stable for the segment. Cigarette volumes declined by just 0.4% last quarter, which the company can make up for through price increases.

Overall, Philip Morris International was able to grow sales by 9.7% year over year in second-quarter 2024, or 11% on an organic, constant-currency basis, to $8.8 billion. It generated $3 billion in operating earnings for an operating margin of 34%.

What’s next for the stock?

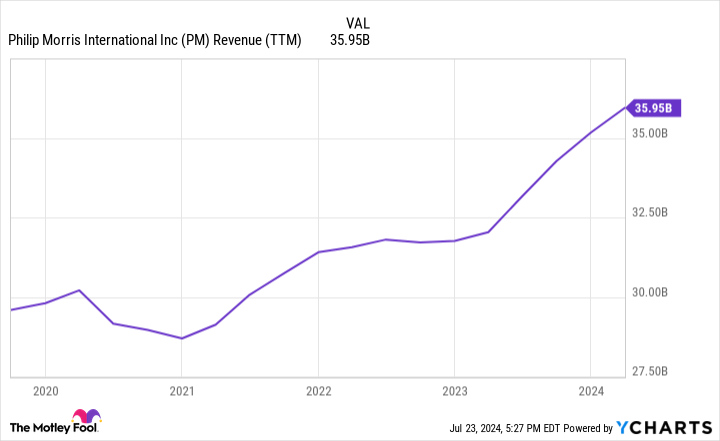

It has been a good start to the year for Philip Morris International. The stock has posted a total return of 17% year to date (YTD) and still trades at a dividend yield of 4.75%. Revenue has started to grow again, hitting $36 billion over the last 12 months.

Operating margin is down, but that is because of the company’s heavy investments in alternative nicotine products such as Zyn and IQOS. Management says that at scale, these products should have similar (if not better) unit economics than legacy cigarettes. Historically, Philip Morris International had an operating margin of 40%.

If the company can hit $40 billion in revenue within five years (only slight growth over the last 12 months) and regain its 40% operating margin, the company will be generating $16 billion in annual earnings. Today, the stock trades at a market cap of $170 billion, or a forward price-to-earnings ratio (P/E) of 10.6 based on these estimates. This looks mighty cheap for long-term shareholders.

Add in the dividend, and I think Philip Morris International stock will continue its strong run over the next five to 10 years and beyond. Buy this stock to play the transition to alternative nicotine products around the globe.

Should you invest $1,000 in Philip Morris International right now?

Before you buy stock in Philip Morris International, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Philip Morris International wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $692,784!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of July 22, 2024

Brett Schafer has no position in any of the stocks mentioned. The Motley Fool recommends Philip Morris International. The Motley Fool has a disclosure policy.

Huge News For Philip Morris International Stock: Here’s What Comes Next was originally published by The Motley Fool