Carry-Trade Blowup Haunts Markets Rattled by Rapid-Fire Unwind

(Bloomberg) — By now, last Monday’s global market meltdown looks more like a brief tremor, a fleeting panic unleashed by a small policy shift from the Bank of Japan and resurgent fears of a US recession.

Most Read from Bloomberg

But the way it unfolded so rapidly — and just as quickly faded out — is exposing how vulnerable markets are to a strategy that hedge funds exploited to bankroll hundreds of billions of dollars of bets in virtually every corner of the world.

The yen carry trade, as it’s known, was a sure-fire recipe for easy profits: Just borrow in Japan, the world’s last haven of rock-bottom interest rates, then plow it into Mexican bonds yielding over 10%, Nvidia’s soaring shares or even Bitcoin. When the yen kept falling, the loans became even cheaper to repay, and the payoffs turned that much bigger.

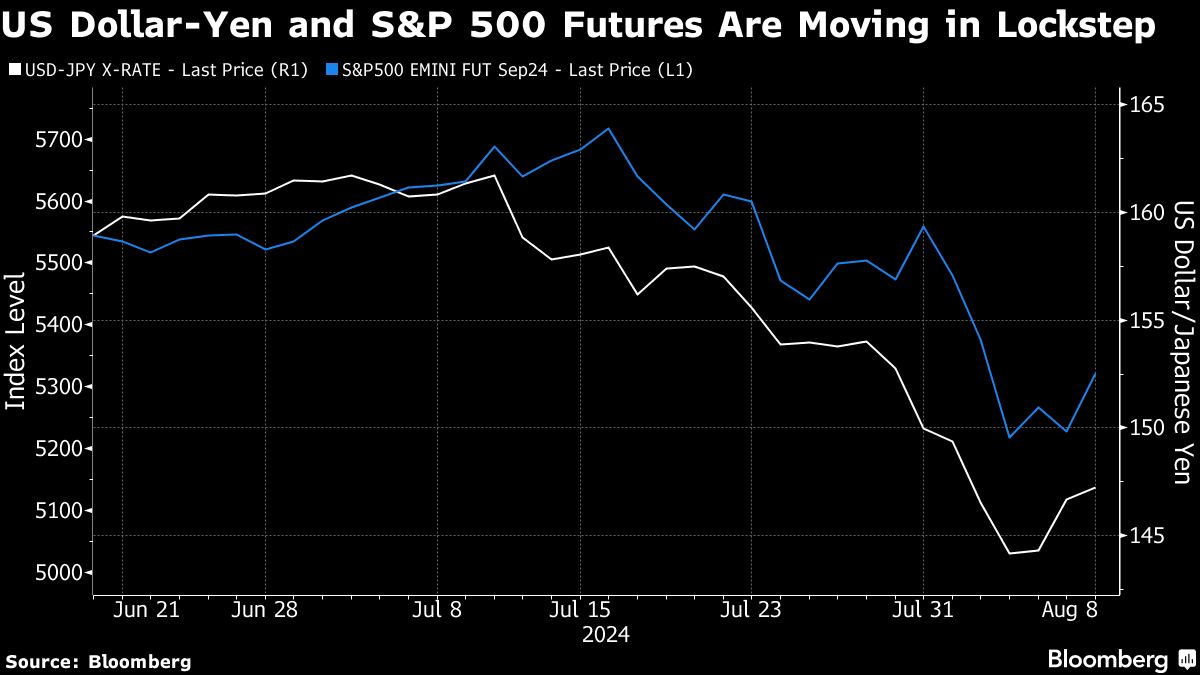

Then, seemingly all at once, investors bailed out of the trade, in turn helping to fuel a furious rebound in the yen and a swift exodus from equities and other currencies as traders dumped assets to meet margin calls. It roiled Japan’s stock market, too, setting off the fiercest one-day selloff since 1987 on concern the surge in the currency would hammer exporters.

“The yen carry trade remains the epicenter of everything in markets right now,” said David Lutz, head of ETFs at JonesTrading.

The pressure had been building up for weeks as markets in carry-trade hot spots sputtered, the Nasdaq 100 Index slid off record highs and worries mounted that the Federal Reserve had kept monetary policy too tight for too long.

Then came the spark: an interest rate hike in Japan. The BOJ’s benchmark is now still a mere 0.25%, the lowest in the industrial world, but the increase at the end of last month was large enough to force investors to rethink their long-held belief that Japanese borrowing costs would always remain pinned near zero.

Even though markets have steadied, the episode is raising alarms about how much leverage had built up around Japan as its central bank kept pumping out cash despite the post-pandemic inflation surge. That’s left anxious traders trying to gauge whether the bulk of the unwinding is over— or whether it will continue rippling through markets in the weeks ahead.

Coming up with an answer is tricky because there are no official estimates for how much money is tied up in carry trades. According to GlobalData TS Lombard, there was some $1.1 trillion piled into the strategy, assuming all overseas borrowing in Japan since the end of 2022 was used to finance it and domestic investors used leverage for their foreign purchases.

After last week’s dramatic unwinding, strategists at JPMorgan Chase & Co. reckoned that three-quarters of global currency carry trades have now been closed out, while those at Citigroup Inc. said the current level of positioning has taken markets out of the “danger zone.”

But others like BNY believe the unwind has further room to run, potentially driving the yen toward 100 to the US dollar — a fall of over 30% from where the currency pair ended last week.

“Further carry-trade unwinding seems likely but the most significant and destructive part of this bubble-burst is now behind us,” Steven Barrow, head of G10 strategy at Standard Bank in London, said in a note to clients last week.

What Bloomberg’s Strategists Say…

“The truth is that the yen is still deeply undervalued, and as the Fed gets going with its policy loosening, those carry trades still left on look increasingly wobbly. But Monday’s episode was entirely about the markets and it isn’t about to cause an adverse feedback loop for the real economy.”

— Ven Ram, macro strategist

See MLIV for more

The bubble, as Barrow called it, has decades-old roots. In the 1990s, with Japan’s economy shadowed by a real estate crash, policymakers there slashed interest rates to zero. The trade has even been blamed by International Monetary Fund economists for playing a part in the 2008 financial crisis.

By 2016, the BOJ had nevertheless pushed rates into negative territory.

The incentive for speculators to borrow in Japan increased once other central banks started racing to contain the steep spike in inflation after the world reopened from the pandemic. As rates were lifted all around the world, the BOJ kept its benchmark beneath zero — widening the profits that could be made on carry trades.

The result was a wave of speculative cash that flowed out of Japan, putting downward pressure on the yen as traders sold the currency to buy those of the countries where they were investing the proceeds.

The impact was particularly stark in Latin America, which offered rates well above those in the US and Europe. In 2022 and 2023, currencies like the Brazilian real and the Mexican peso rose sharply, becoming some of the world’s best performers.

By one measure, borrowing in the yen and investing in Mexico, for example, produced returns of 40% last year alone. The strategy continued to rack up gains, with yen-funded trades in a basket of eight emerging-market currencies returning just over 17% this year to early July.

“To go long the peso was such a no-brainer just a few months ago — but those days are definitely behind us,” said Alejandro Cuadrado, head of global FX and Latin America strategy at Banco Bilbao Vizcaya Argentaria SA in New York.

When the yen started rebounding sharply from its weakest levels in decades, that created a feedback loop as traders unwound carry trades to lock in their gains — pushing the yen up further as investors purchased it to close out their loans. It accelerated after the BOJ hiked rates on July 31 for a second time this year and surprisingly weak US job figures fanned fears that the Fed had waited too long to reverse course.

After the unwind hit Japan’s stock market on Aug. 5, driving the Nikkei down 12%, BOJ Deputy Governor Shinichi Uchida stepped in to assure investors the central bank won’t be raising rates as long as market instability persists. The markets steadied, with signs that hedge funds pulled back some bets that the yen would continue to gain.

The recent turn has, at least temporarily, likely tamped down the carry trade, with traders anticipating more volatility in foreign exchange markets this year.

“No trade lasts forever — and, the facts have changed,” said Jack McIntyre, a senior portfolio manager at Brandywine Global Investment Management. “The BOJ tightened and something broke — in this case the carry trade.”

–With assistance from Srinivasan Sivabalan, Zijia Song, Tania Chen, Ruth Carson, Catherine Bosley and Jessica Menton.

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.