Banks don’t want to inspect your home office, so they’re forcing hundreds of employees to come in five days a week

Renewed rules for workplace inspections every few years are being blamed for mass return-to-office efforts.

Work-from-home regulations for banks are changing, and some of the industry’s biggest players would rather bring employees in five days a week than make the effort to comply—including making regular inspections of workers’ homes.

During the pandemic, brokerage industry watchdog the Financial Industry Regulatory Authority (FINRA), suspended rules on workplace inspections to make it easier for banks to allow their employees to work from home. The agency is now moving back to its pre-pandemic requirements for monitoring workplaces, meaning some home offices will have to be registered with regulators and remotely inspected at least every three years under a new pilot program.

Now, some of the banks that had been most flexible with their work-from-home policies, including Citigroup, Barclays, and HSBC, have decided complying with the renewed rules isn’t worth the effort, Bloomberg reported. Between them, the three banks are bringing thousands of their workers back to the office five days a week.

Citigroup said that it would require 600 employees previously eligible to work from home to come into the office five days a week, although it said in a statement that most of its staff can still work remotely two days a week, per the outlet. Barclays cited “new regulatory policies” in a memo as part of why it is bringing thousands of its investment banking employees worldwide back to five days a week in person. And 530 of HSBC’s New York workers may need to change their remote-work habits soon as well, Mabel Rius, head of human resources for the U.S. and Americas, told Bloomberg.

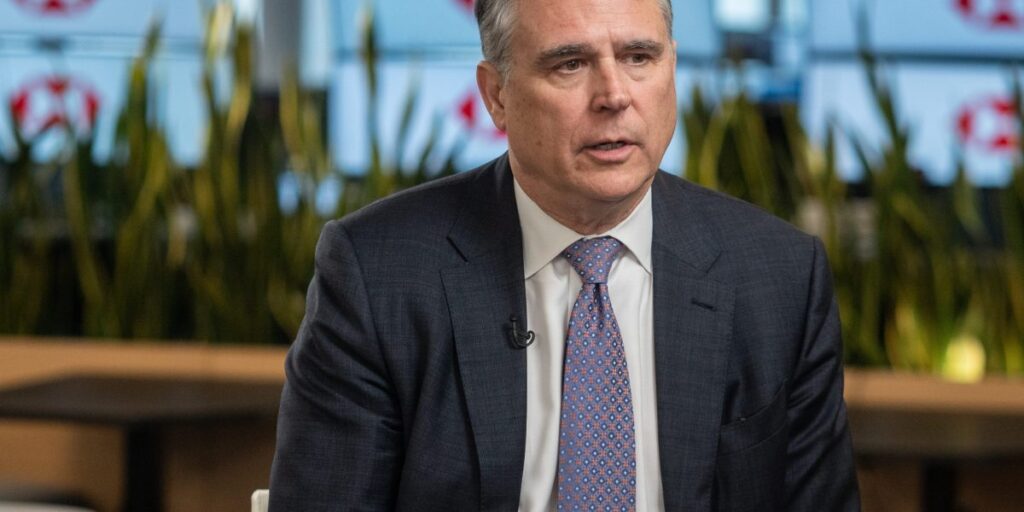

Michael Roberts, HSBC CEO of the U.S. and Americas, told Bloomberg that while the bank will comply with the FINRA regulations, he wants employees to want to come back to the office.

“What we did not want to do is to force people to come back simply out of decree,” Roberts told Bloomberg in an interview.

Part of enticing employees to work in person means listening to why they like coming to the office at all. Roberts said the bank has incorporated much of that input at its new U.S. headquarters in New York City’s Hudson Yards, to make it “conducive to people coming back.”

“We will adjust to the FINRA rules. We’ll make sure that whoever needs to be there five days a week will be here five days a week, but I don’t want to decree people coming back,” Roberts said. “I want them to come back because they want to come back.”

Meanwhile, some of the industry’s other giants, including Bank of America and Goldman Sachs, have already handed down mandates for five-day in-person weeks.

JPMorgan Chase CEO Jamie Dimon, perhaps the best-known CEO on Wall Street, has long been critical of remote work. Last year, the bank instituted mandatory return-to-office policies for senior employees, and Dimon said earlier this year that about 60% of the bank’s workers were on-site full-time.

FINRA, for its part, disputed that its renewed policies were to blame for stricter work-from-home policies by banks. The regulator said in a statement that some of its rules weren’t any stricter than they were prior to the pandemic, and that, in fact, it adjusted some rules, including allowing remote workplace inspections. Those changes “provide member firms greater flexibility—not less—to allow eligible registered persons to work from home,” FINRA said.

“FINRA has seen recent statements from firms stating that new, stringent rules from FINRA will require them to bring their workforce back to the office full time,” it wrote in the statement. “This is incorrect.”

A version of this story originally published on Fortune.com on May 25, 2024.