All Social Security Retirees Should Do This on Oct. 10

Are Social Security benefits an important piece of your retirement income? If so, you might want to keep your eyes and ears open on Thursday, Oct. 10. That’s when the cost-of-living adjustment for the coming year’s monthly payments will be announced. These increases are intended to maintain retirees’ buying power by keeping pace with inflation.

Of course, sometimes they’re still not quite enough.

To this end, it wouldn’t be wrong to start thinking about your bigger financial picture for the coming year. Whether or not the impending increase in Social Security’s payments is fair and reasonable, there are some strategic actions investors may want to consider taking in the meantime.

Retirees, mark your calendars

If you’re a retiree who’s feeling a bit cash-strapped these days, you’re not alone. Although the Social Security Administration upped its average payout by 3.2% in January of this year (roughly $58 per month), prices have continued to rise in the meantime. The Bureau of Labor Statistics reports that consumers’ costs have grown on the order of 2% since the end of 2023. For elderly individuals who may spend more than younger people do on services like healthcare, costs are up closer to 3%.

If you’re on a budget, these nickels and dimes add up.

Fortunately, this inflation is more or less in line with the expected cost-of-living adjustment (or COLA) increase. While the Social Security Administration doesn’t provide any official forecasts, The Senior Citizens League’s most recent prediction suggests the COLA for 2025’s Social Security payments will be a respectable 2.5%. That expected increase is down slightly from projections made earlier in the year although inflation has cooled a bit in the meantime.

Whatever the final increase ends up being, the Social Security Administration will be reporting it at its website on Thursday, Oct. 10. There’s little doubt that most of the financial media industry will be widely sharing the news shortly thereafter.

Of course, as a retired (or soon-to-be retired) investor, your goal is to not need to sweat this particular number too much either way. You should aim to do even better with your own income-generating investments. On that note:

3 things every retiree should do regardless

Social Security was never meant to be the entirety of anyone’s retirement income. With an average monthly payment of just over $1,900, it’s almost unlivable on its own. You’ll likely want (and need) to supplement this income. That means saving and investing money in your working years, and then making the most of it when the time comes.

If you’re watching for these annual COLA numbers then you’re likely already at least semi-retired, and probably not adding any meaningful amount of money to your retirement nest egg. That doesn’t mean you shouldn’t take a fresh look at the money you’ve got saved up, though. You might want to think about doing the following no matter what the Social Security Administration announces on Thursday.

1. Lock in interest rates on bonds before interest rates sink any further

Bond investors living on their interest income should first and foremost build what’s called a bond ladder. That just means arranging the maturity dates on all of your fixed-income investments (Treasuries, CDs, corporate bonds, etc.) so they’re evenly staggered from the next few weeks to the next several years. Such a structure hedges your bond portfolio’s unique risks while also insuring your net interest payments remain relatively stable over time.

On the flip side, the Federal Reserve has plainly said it foresees at least 100 basis points’ worth of reduction in the federal funds rate between now and next year, with less aggressive rate cuts in the cards the year after that. Although interest rates on the aforementioned fixed-income instruments have already fallen thanks to last month’s 50 basis point cut, they’ll likely be falling again soon.

It wouldn’t be wrong to overload certain maturity rungs of your bond ladder with more higher-yielding holdings than you might normally choose to hold. (Just don’t go crazy — basic diversification is still important.)

2. Re-examine all of your dividend-paying stocks

It’s easy to conclude the stock market’s higher-yielding stocks are the best choice for income-minded investors. That’s not necessarily the case, though. It’s not uncommon for higher-yielding dividend stocks to log anemic increases in their payouts — presuming they offer any actual dividend growth at all. For instance, while Kraft Heinz boasts a healthy forward-looking dividend yield of 4.5%, the consumer staples company hasn’t raised its quarterly per-share payment of $0.40 since the beginning of 2020. Patient shareholders are actually losing buying power.

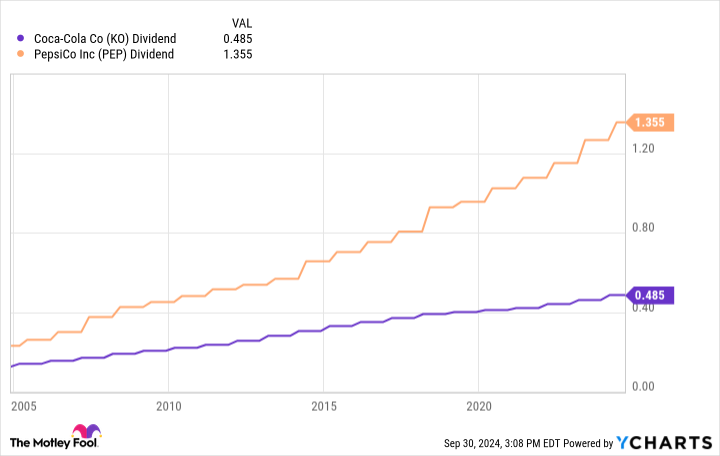

Then there are the less obvious ill-advised decisions. Take Coca-Cola and PepsiCo as examples. While Coca-Cola tends to be the preferred investment of the two due to its greater stature, PepsiCo’s forward-looking dividend yield of 3.2% is actually better than Coke’s dividend yield of 2.7%. PepsiCo also boasts stronger dividend growth than its bigger rival.

Given how Social Security’s inflation-matching cost-of-living adjustments mean no recipient ever makes any actual net progress in terms of the spendable income it provides, investors will only be able to achieve this on their own — with their own savings. It pays to make the most of it.

3. Compare your spending to your portfolio’s income-generating potential

Last but not least, you’ll want to figure out how much money you’ll actually be spending next year, and then determine if your current portfolio is even capable of generating that amount (without compromising its ability to do the same in the future).

Yes, holding the right stocks and bonds is part of the equation. But it’s not the only part. The allocation is a factor as well. Can you meet your near-term goals and still reach your long-term goals with fewer stocks and more bonds? Is it possible you need more capital appreciation from your dividend-paying stocks?

There’s still more to the story. Given that Social Security’s COLAs don’t always seem to fully keep pace with retirees’ actual increases in living costs, you may need to rethink and reset your retirement spending plans as well. Are you really watching all of those streaming channels on a regular basis? Perhaps its time to make a call about your automobile insurance options. Maybe you can forego one of your regular restaurant visits. As was noted above, the nickels and dimes can add up over the course of a year.

Whatever you need to do, just be ready for the big news on Oct. 10.

The $22,924 Social Security bonus most retirees completely overlook

If you’re like most Americans, you’re a few years (or more) behind on your retirement savings. But a handful of little-known “Social Security secrets” could help ensure a boost in your retirement income. For example: one easy trick could pay you as much as $22,924 more… each year! Once you learn how to maximize your Social Security benefits, we think you could retire confidently with the peace of mind we’re all after. Simply click here to discover how to learn more about these strategies.

View the “Social Security secrets” »

James Brumley has positions in Coca-Cola. The Motley Fool recommends Kraft Heinz. The Motley Fool has a disclosure policy.

All Social Security Retirees Should Do This on Oct. 10 was originally published by The Motley Fool