Coca-Cola Is a Rock-Solid Dow Dividend Stock, but So Is This Dividend King That Plans to Pay $10 Billion in Dividends Over the Next Year.

It’s been a volatile week or so for Procter & Gamble (NYSE: PG), which fell up to 6% in response to its fourth-quarter fiscal 2024 results, only to make up those losses and rise to near an all-time high. It’s a lesson in why knee-jerk reactions to quarterly earnings can be misleading.

Here’s a breakdown of where P&G stands, what it expects from fiscal 2025, and why the dividend stock is worth buying now.

Titans of dividend growth

Coca-Cola is one of the most well-known dividend stocks out there. It has paid and raised its dividend for 62 consecutive years, making it a Dividend King. Dividend Kings have at least 50 consecutive years of dividend raises. Coke stock just hit an all-time high as it sustains high margins and works to boost volumes.

The beverage king pays around $8 billion in dividends a year — giving it one of the highest dividend expenses in the S&P 500. But it still doesn’t pay as much as Procter & Gamble. In April, P&G raised its dividend by 7% — marking the 68th consecutive year it increased the dividend. The streak makes P&G one of the longest-tenured Dividend Kings.

In fiscal 2024, P&G paid $9.3 billion in dividends and made $5 billion in share repurchases. In its recent earnings report, P&G gave fiscal 2025 guidance that forecasts a whopping $10 billion in dividend payments and $6 billion to $7 billion in stock repurchases. The guidance suggests that another sizable dividend raise could be coming, and that P&G feels it can support a growing capital return program.

The pace at which P&G is raising the dividend is a significant vote of confidence for passive income investors. P&G is hyper-aware of the importance of its dividends and buybacks to the investment thesis. Investors expect annual dividend raises, meaning every time P&G raises the dividend, it effectively sets the bar higher for the following year’s obligation.

For Dividend Kings, dividend raises work the same way as compound interest. A 7% raise may not sound like much at first glance — but 7% of $9 billion is $630 million. The difference in dividend expense from one year to the next is basically the amount of extra earnings P&G has to make to keep the same payout ratio. It’s a tall order — which is why there are only around 50 Dividend Kings — and very few of them have as attractive of a dividend or buyback program as P&G.

P&G’s focus remains on margins

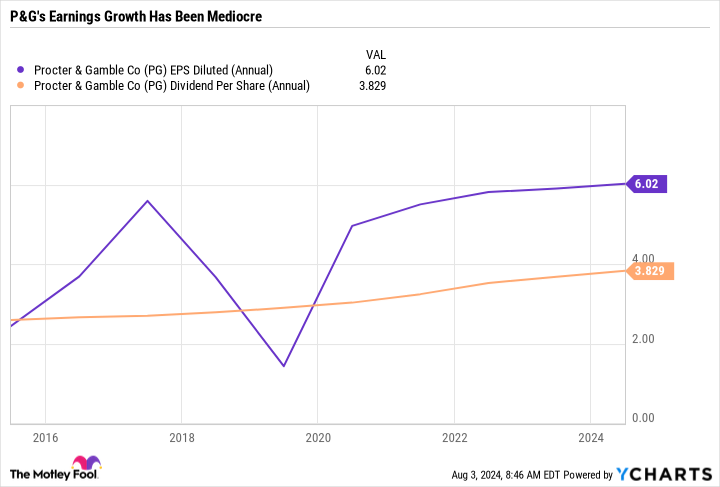

Procter & Gamble’s fiscal 2025 forecast paints a rosy picture of where the dividend is headed. But long-term investors may want to ask whether the business can really sustain this pace of raises, or if P&G is setting itself up to be pressured down the road. P&G’s earnings growth has — admittedly — been fairly disappointing in recent years.

As the chart shows, the dividend has steadily climbed, but earnings are only slightly higher today than in fiscal 2017. However, P&G still has a reasonable payout ratio and generates plenty of extra earnings to support its buyback program and reinvest in the business. There’s also reason to believe that P&G is headed in the right direction to support future earnings growth.

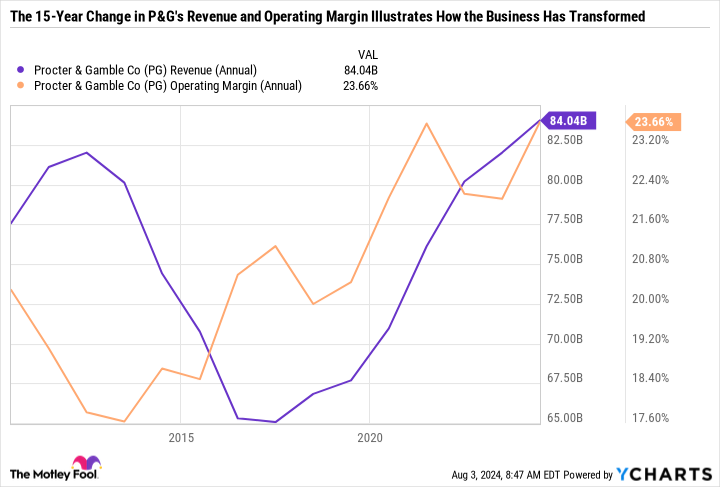

P&G underwent a significant turnaround between fiscal 2015 and 2017, which reduced its brand count by around 60%. The objective was to focus on the best brands and improve margins — even at the expense of sales. The strategy was a resounding success.

Today, P&G is a high-margin cash cow that focuses more on profitability than sales. This chart illustrates just how much P&G’s sales dropped during its restructuring, as well as the significant margin expansion and sales growth it has enjoyed in recent years.

As for the current state of the business, P&G successfully raised prices to combat inflation over the last few years. However, it has experienced lackluster volumes — which has impacted its growth. Despite flat volume growth, P&G has delivered just 4% organic sales growth in fiscal 2024. It expects just 3% to 5% organic sales growth in fiscal 2025 and 5% to 7% core EPS growth.

The forecast is OK, but not great. However, P&G provided some added context on the earnings call. It expects the first half of fiscal 2025 to resemble fiscal 2024, but is confident it can reaccelerate volume growth and hold or build upon margins.

In other words, P&G is making a strategic decision not to drastically cut prices at the expense of its margins just to drive sales growth. This is a fairly different strategy than companies like McDonald’s or PepsiCo, which are tapping into cost-conscious consumers through value options. P&G may pull back on the pace of price hikes, but it is unlikely to make sweeping price cuts to spur volume growth.

P&G is a super-safe dividend stock to buy now

There are plenty of higher-yield options out there than P&G, which yields just 2.4%. And with a 28.3 price-to-earnings ratio, P&G is fairly expensive compared to other, more value-oriented choices in the consumer staples sector. Yet, P&G continues to prove why it is worth the premium price tag.

It starts by understanding that P&G could sport close to a 4% yield if it didn’t repurchase stock. But stock buybacks are a core element of the capital return program and have been instrumental in helping reduce the outstanding share count and keep P&G a decent value despite the strong performance of its stock price.

P&G also has incredible pricing power, as evidenced by management’s confidence that it can retain high margins and gradually work toward boosting volumes without the need to overhaul its strategy just because consumer spending is tight.

With P&G stock near an all-time high, investors certainly have to pay up for it. But if you prefer buying a high-quality business at an expensive price rather than a mediocre business at a great price, then P&G is worth a closer look.

Should you invest $1,000 in Procter & Gamble right now?

Before you buy stock in Procter & Gamble, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Procter & Gamble wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $606,079!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of August 6, 2024

Daniel Foelber has positions in McDonald’s. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

Coca-Cola Is a Rock-Solid Dow Dividend Stock, but So Is This Dividend King That Plans to Pay $10 Billion in Dividends Over the Next Year. was originally published by The Motley Fool