MicroStrategy’s 10-for-1 Stock Split Is Imminent: 10 Things You Need to Know

Though there’s little doubt Wall Street is enamored with the rise of artificial intelligence (AI), the return of stock-split euphoria has given investors another reason to cheer.

A stock split gives publicly traded companies the ability to alter their share price and outstanding share count by the same factor. Over the last six months, 12 time-tested companies have announced or completed a stock split.

Stock splits can occur in either direction. A reverse split is designed to increase a company’s share price, usually with the purpose of ensuring that it continues to meet the minimum listing standards of a major stock exchange. On the other hand, a forward-stock split is conducted by companies wanting to reduce their nominal share price. Since forward splits are almost universally undertaken from a position of strength, this is the type of split most investors tend to flock to.

Following the recent 10-for-1 forward split for Nvidia, historic 50-for-1 split for Chipotle Mexican Grill, and 10-for-1 split for AI networking solutions specialist Broadcom, the time has come for MicroStrategy (NASDAQ: MSTR) to join the “Class of 2024” stock-split stocks.

Here are the 10 things you need to know about MicroStrategy’s imminent stock split.

1. This is a history-making stock split for MicroStrategy

On July 11, MicroStrategy broke the news that it would be conducting a forward split. With its share price firmly in the $1,300s, the company’s board approved a historic 10-for-1 stock split.

This marks the third split in the company’s history since going public in June 1998, and is its largest forward split, following a 2-for-1 forward split in January 2000 and a 1-for-10 reverse split in July 2002, during the dot-com bubble.

2. It goes into effect following the close of trading today

The use of the word “imminent” in the headline isn’t hyperbole. Following the close of trading today, August 7, MicroStrategy’s 10-for-1 forward split will be effective. Based on where things ended on August 2, the company’s share price will decline to around $145, while its outstanding share count will increase tenfold.

Keep in mind that some online brokerages might fail to recognize that a split has occurred for up to 24 hours. In other words, shareholders shouldn’t panic if they see a large, unexplained loss in their portfolio on Thursday morning.

3. Stock splits are entirely cosmetic

While the euphoria associated with stock splits is real, and companies enacting forward splits have, on average, outperformed the benchmark S&P 500 in the 12 months following their split announcement (dating back to 1980), stock splits themselves are entirely cosmetic events.

Though a split changes a company’s share price and outstanding share count, it doesn’t alter its market cap or have any impact on its underlying operating performance.

4. MicroStrategy’s split is all about accessibility (and retail investors)

According to the company, the all-important “Why?” behind this split is to “make MicroStrategy’s stock more accessible to investors and employees.” For retail investors and employees without access to fractional-share purchases, it takes almost $1,450 to buy a single share of stock. By tomorrow, investors will only need around $145 to buy one share.

Although some online brokers offer access to fractional-share purchases, MicroStrategy’s stock has, arguably, been driven higher by retail investors more than any other Class of 2024 stock-split stock. Reducing its share price to a retail investor-friendly level is imperative to maintaining interest from MicroStrategy’s key supporters.

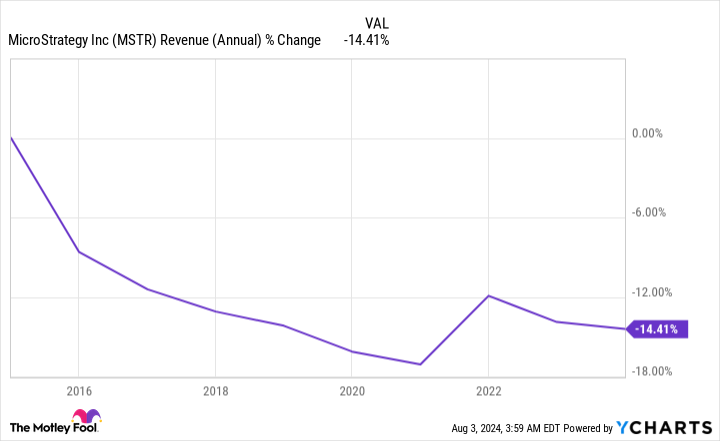

5. It’s, technically, an AI-driven software company

For decades, software has been MicroStrategy’s foundational operating segment. Management is betting on artificial intelligence to provide a spark to its enterprise analytics software segment, which has seen sales slump by 14% over the last decade (as of the end of 2023).

If there’s a silver lining, it’s that subscription services revenue has been climbing by a double-digit percentage on a year-over-year basis. Unfortunately, this hasn’t halted the company’s aggregate software sales decline or segment operating losses.

6. MicroStrategy is the largest corporate holder of Bitcoin

But let’s be honest: Investors aren’t buying MicroStrategy stock because of AI-driven enterprise analytics software. They’re purchasing shares because it’s the largest corporate holder of Bitcoin (CRYPTO: BTC), the leading cryptocurrency by market value.

As of July 31, the company held 226,500 Bitcoins, which equates to more than 1% of the 21 million tokens that will ever be mined. Cryptocurrency enthusiasts and Bitcoin supporters have flocked to MicroStrategy as an easy way to bet on the success of this digital gold.

7. Its Bitcoin assets are being valued at a nearly 90% premium

Investors have been a bit overzealous in their pursuit to own shares of MicroStrategy. At the time of this writing, a single Bitcoin was worth about $61,400. This means the company’s Bitcoin assets have a value of around $13.8 billion.

The problem is that MicroStrategy’s market cap on August 2 was $27.6 billion. Backing out a fair value for its money-losing software operations shows that investors are paying a roughly 90% premium to Bitcoin’s actual token price to own shares of MicroStrategy. In other words, instead of buying Bitcoin for $61,400 per token on a crypto exchange, investors are paying closer to $116,000 per token for the assets in MicroStrategy’s Bitcoin portfolio. This premium doesn’t make any sense.

8. The company has financed its Bitcoin purchases with convertible-debt offerings

Something else that’s clearly a concern is how Bitcoin-enthusiast CEO Michael Saylor has been facilitating the steady purchase of the world’s largest cryptocurrency. On numerous occasions, MicroStrategy has sold convertible debt, which it’s used to buy Bitcoin.

While this is a strategy that can work wonders during crypto bull markets, it’s akin to playing with fire during long-winded bear markets. Bitcoin has endured multiple 80% (or greater) drawdowns in its relatively short existence. Being heavily levered to Bitcoin with convertible debt and minimal operating cash flow from its software operations is a disaster waiting to happen.

9. The world’s largest cryptocurrency has, arguably, lost many of its first-mover advantages

Although Bitcoin has undeniably benefited from its first-mover advantages, the digital gold that MicroStrategy has tethered its future to has, arguably, given up a lot of these advantages as time has passed. Numerous blockchain projects and crypto-based payment networks offer faster payment validation and lower transaction costs.

Furthermore, Bitcoin’s real-world utility experiment has failed to pass muster. Despite repeated efforts by El Salvador’s regulators to encourage its residents to use Bitcoin as legal tender, approximately 7 out of 8 El Salvadorans didn’t transact with Bitcoin last year.

10. MicroStrategy stock should be avoided by investors

The 10th and most-important thing to know is that stock-split euphoria eventually fades. When that happens, investors will be left with an over-levered company tied to a volatile asset that’s lost many of its first-mover advantages.

If you disagree with me and believe Bitcoin is going to head higher, there are a lot of ways to invest in it. Paying a 90% premium to the current price of Bitcoin by purchasing shares of MicroStrategy is probably the worst way to do it.

Should you invest $1,000 in MicroStrategy right now?

Before you buy stock in MicroStrategy, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and MicroStrategy wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $615,516!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of August 6, 2024

Sean Williams has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Bitcoin, Chipotle Mexican Grill, and Nvidia. The Motley Fool recommends Broadcom and recommends the following options: short September 2024 $52 puts on Chipotle Mexican Grill. The Motley Fool has a disclosure policy.

MicroStrategy’s 10-for-1 Stock Split Is Imminent: 10 Things You Need to Know was originally published by The Motley Fool