Treasuries Surge as Traders Bet Big on a Fed Rescue Move

(Bloomberg) — Bond traders are piling into bets that the US economy is on the verge of deteriorating so quickly that the Federal Reserve will need to start easing monetary policy aggressively to head off a recession.

Most Read from Bloomberg

Previous worries about the risk of elevated inflation have virtually disappeared, swiftly giving way to speculation that growth will stall unless the central bank starts pulling interest rates down from a more than two-decade high.

That is fueling one of the biggest bond-market rallies since fears of a banking crisis flared in March 2023. The advance has been so strong that the policy sensitive two-year Treasury yield tumbled last week by half a percentage point to less than 3.9%. It hasn’t been that far below the Fed’s benchmark rate — now around 5.3% — since the global financial crisis or the aftermath of the dot-com crash.

The moves extended in Asia trading Monday with two-year yields slumping more than 10 basis points to 3.77% as bonds rallied across the curve.

“The market concern is that the Fed is lagging and that we are morphing from a soft landing to a hard landing,” said Tracy Chen, a portfolio manager at Brandywine Global Investment Management. “Treasuries are a good buy here because I do think the economy will continue to slow.”

Bond traders have repeatedly misjudged where interest rates have been headed since the end of the pandemic, however, at times overshooting in both directions and caught off guard when the economy bucked recession calls or inflation defied expectations. At the end of 2023, bond prices also surged on conviction that the Fed was poised to start easing policy, only to give back those gains when the economy kept exhibiting surprising strength.

So there’s a chance that the latest move is another such swing too far.

“The market is overshooting and getting ahead of itself like we saw late last year,” said Kevin Flanagan, head of fixed income strategy at WisdomTree. “You need validation from more data.”

But sentiment has shifted sharply after a string of data showed a softening job market and cooling in segments of the economy. On Friday, the Labor Department reported that employers created just 114,000 jobs in July, far short of what economists were forecasting, and the unemployment rate unexpectedly rose.

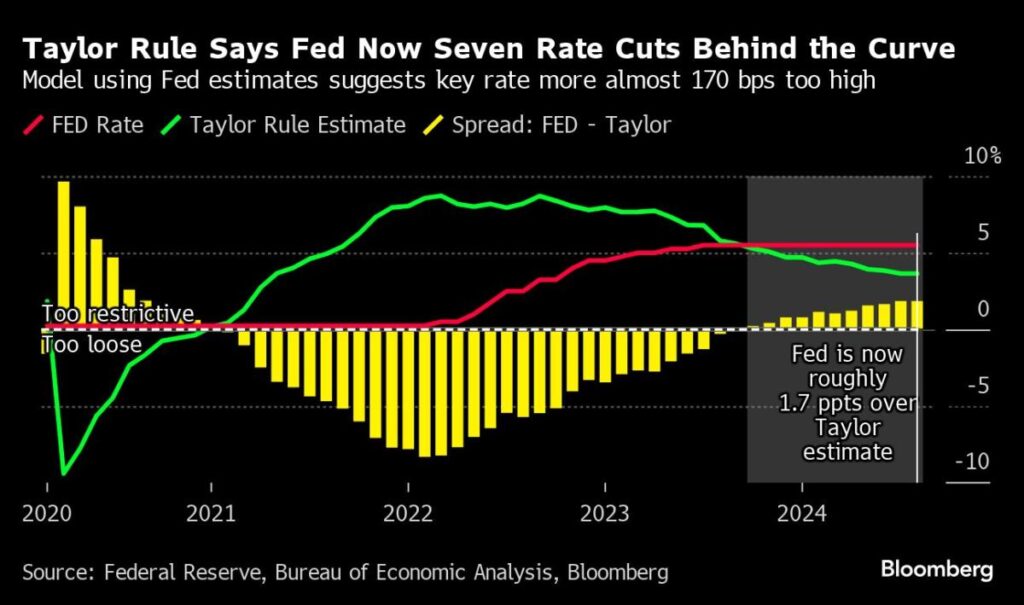

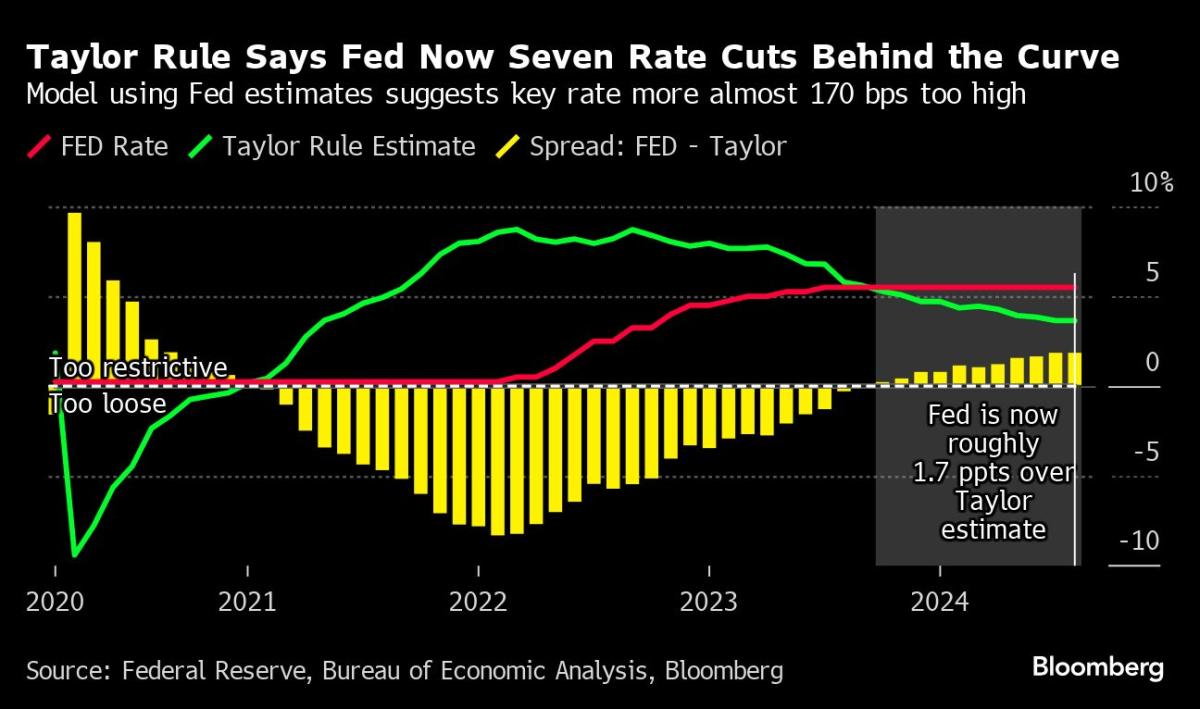

After the Fed on Wednesday again held rates steady, the data fanned worries that the central bank has been too slow to react — just as it was in raising interest rates once inflation lingered well after the economy reopened from the pandemic. That’s been reinforced by the fact that central banks in Canada and Europe have already started easing policy.

Fears of a slowing economy and Fed delays have contributed to a sharp selloff in US stocks last week, with sentiment further dented over the weekend after Berkshire Hathaway Inc. slashed its stake in Apple Inc. by almost 50% as part of a massive second-quarter selling spree.

“There’s been an absolutely enormous move in the 2-year yield in the past 10 days or so. It’s hard to price a so-called safe-haven asset, it’s much harder to price riskier assets – stocks,” said Steve Sosnick, chief strategist at Interactive Brokers LLC. “And Warren Buffett’s decision to lighten up his Apple position doesn’t help things from a sentiment perspective.”

Deeper Cuts

Economists across Wall Street have started anticipating a more aggressive pace of Fed easing, with those at Citigroup Inc. and JPMorgan Chase & Co. predicting half-percentage-point moves at the September and November meetings.

On Sunday, Goldman Sachs Group Inc. economists increased the probability of a US recession in the next year to 25% from 15%, but said there are several reasons not to fear a slump.

The economy continues to look “fine overall,” there are no major financial imbalances and the Fed has a lot of room to cut rates and can do so quickly if needed, the economists said.

Futures traders are pricing in roughly the equivalent of five quarter-point cuts through the end of the year, indicating expectations for unusually large half-point moves over the course of its last three meetings. Downward moves of that scale haven’t been enacted since the pandemic or the credit crisis.

The Treasury rally drove the benchmark 10-year yield — a key baseline for borrowing costs across markets — to about 3.8%, the lowest since December. The advance was supported by the slide in the stock market on the heels of some weak earnings reports from companies like Intel Corp., which announced it is cutting thousands of jobs.

What Bloomberg Strategists say…

“Locking in yield is clearly a priority for bond investors as more evidence of jobs deterioration means rate cuts are coming, potentially fast and furiously in the next several months. Friday’s jobs report has given bond markets pause about that framing and intensified worries the Fed is now making a policy mistake.”

—Edward Harrison, strategist. Read more on MLIV

Kathryn Kaminski, chief research strategist and portfolio manager at quant fund AlphaSimplex Group, said there appears to be room for bonds to continue to gain, given the downturn in the stock market and a push by investors snap up bonds before yields fall even more. She said the firm’s trend-following signals turned them bullish on bonds this month after previously being bearish.

“People wanting to lock in rates creates a lot of buying pressure and there’s also risk-off going on,” said Kaminski. “The 10-year yield could go down to closer to 3% if we do get these Fed rate cuts by the end of the year.”

What to Watch

-

Economic data:

-

Aug. 5: S&P Global US services and composite PMIs; ISM services index

-

Aug. 6: Trade balance

-

Aug. 7: MBA mortgage applications; consumer credit

-

Aug. 8: Initial jobless claims; wholesale trade sales and inventories

-

-

Fed calendar:

-

Auction calendar:

-

Aug. 5: 13-, 26-week bills;

-

Aug. 6: 52-week bills; 42-day CMB; three-year notes

-

Aug. 7: 17-week bills; 10-year notes

-

Aug. 8: 4-, 8-week bills

-

–With assistance from Stephen Kirkland.

(Updates with moves Monday)

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.