The Sahm rule and the economy’s ‘statistical regularities’

A version of this post first appeared on TKer.co.

Just because something happened a bunch of times in the past doesn’t mean it must happen again in the future.

This is what Fed Chair Jerome Powell communicated when asked about the “Sahm Rule” recession indicator, which has revealed that recessions historically started when the three-month moving average of the unemployment rate rose 0.5 percentage points or more above its 12-month low.

“A statistical regularity is what I call it,” Powell said on Wednesday. “It’s not like an economic rule, where it’s telling you something must happen.”

Claudia Sahm, the economist whom the indicator is named after, would agree.

“Indicators of economic downturns like the Sahm rule are empirical regularities from the past, not laws of nature,” Sahm wrote last November.

On Friday, we learned that the unemployment rate rose to 4.3% in July. This caused the three-month moving average of the unemployment rate to breach that 0.5 percentage point threshold for the first time in this economic cycle.

Sahm has been arguing that her namesake indicator triggering could be a false positive due lingering pandemic-related economic distortions.

“The Sahm rule is likely overstating the labor market’s weakening due to unusual shifts in labor supply caused by the pandemic and immigration,” Sahm recently said.

The economy is more than a few metrics

All of this speaks to TKer’s Rule No. 1 of analyzing the economy: Don’t count on the signal of a single metric.

It’s a lesson that’s been learned following false positive recession signals from the yield curve and the Conference Board’s Leading Economic Index.

The economy is complex with countless numbers of moving parts, and sometimes some of those parts will be behaving so abnormally that it will force time-tested indicators to break down.

For example, the current economic cycle has come with an unusually high number of job openings: a sign of abnormally strong demand. At its peak in March 2022, there was an unprecedented two job openings per unemployed person.

Over the past two years, this excess demand for jobs had people controversially believing that it would be possible to bring down inflation without a large rise in unemployment. Because, basically it was those extra job listings that were emboldening workers to press for higher pay, and employers obliged because of booming demand. All the Fed had to do was cool the economy just enough that demand would come down just enough for employers to take down those job listings, the argument went, which in turn would help inflation to come down.

This challenged the traditional understanding that falling job openings comes with higher unemployment — a relationship illustrated by the Beveridge curve — and that higher unemployment is needed to bring inflation down — a relationship illustrated by the Phillips curve.

This is not to say that the Sahm rule, the Beveridge curve, and the Phllips curve are all useless.

The takeaway here is to remember that the economy is complex, and we should keep an eye out for developments that may challenge what have been statistical regularities.

But make no mistake: The labor market is cooling

Just because popular recession indicators are sending false positives doesn’t mean the risk of recession isn’t elevated and that the economy isn’t cooling.

On the contrary, economic activity growth has been decelerating significantly, with labor market metrics normalizing.

This week we’ve learned that job creation continues to cool, the unemployment rate rose to its highest level since October 2021, and the ratio of job openings to unemployed people fell to a three-year low. The quits rate is also down, initial claims for unemployment insurance are up, wage growth is cooling, and labor market confidence is down. And manufacturers expect further deceleration in hiring. For more details, scroll down to TKer’s weekly review of the macro crosscurrents.

Broadly speaking, the economy has been looking a lot less “coiled,” with many signs of excess demand fading.

All this puts increasing amounts of pressure on the Federal Reserve to loosen monetary policy to help the economy avoid recession.

While recession may not be the baseline scenario, it’s prudent to remember that they are normal and they can be rough for stocks in the near-term.

CFRA raises its target for the S&P 500

On Wednesday, CFRA’s Sam Stovall raised his 12-month target for the S&P 500 to 6,145 from 5,610. He noted this implies a year-end level of 5,770. This is his third revision from his initial target.

“What’s more, CFRA equity analysts’ market cap-weighted 12-month target prices for S&P 500 constituents point to a near-14% potential appreciation for the benchmark in the year ahead,” Stovall said.

Stovall is not alone in tweaking his forecast. His peers at Barclays, RBC, Oppenheimer, Yardeni, Citi, Capital Economics, Goldman Sachs, UBS, Morgan Stanley, Deutsche Bank, BMO, HSBC, Societe Generale, and BofA are among those who’ve also raised their targets.

Don’t be surprised to see more of these revisions as the S&P 500’s performance, so far this year, has exceeded many strategists’ expectations.

Reviewing the macro crosscurrents

There were a few notable data points and macroeconomic developments from last week to consider:

Fed holds rates steady, sees risks to both inflation and employment. The Federal Reserve announced it would keep its benchmark interest rate target high at a range of 5.25% to 5.5%.

From the Fed’s statement (emphasis added): “Recent indicators suggest that economic activity has continued to expand at a solid pace. Job gains have moderated, and the unemployment rate has moved up but remains low. Inflation has eased over the past year but remains somewhat elevated. In recent months, there has been some further progress toward the Committee’s 2% inflation objective. The Committee seeks to achieve maximum employment and inflation at the rate of 2% over the longer run. The Committee judges that the risks to achieving its employment and inflation goals continue to move into better balance. The economic outlook is uncertain, and the Committee is attentive to the risks to both sides of its dual mandate.“

For a while, the Fed has been primarily concerned with inflation. With labor market metrics now more in balance, the central bank is now also more concerned about rising unemployment.

This echoes what Fed Chair Powell said to Congress earlier in July: “Reducing policy restraint too late or too little could unduly weaken economic activity and employment.“

That said, Powell’s language during Wednesday’s press conference suggests a rate cut could be coming soon.

“The question will be whether the totality of the data, the evolving outlook, and the balance of risks are consistent with rising confidence on inflation and maintaining a solid labor market,” Powell told reporters Wednesday. “If that test is met, a reduction in our policy rate could be on the table as soon as the next meeting in September.”

That next meeting is scheduled for September 17-18.

The labor market continues to add jobs. According to the BLS’s Employment Situation report released Friday, U.S. employers added 114,000 jobs in July. It was the 43rd straight month of gains, reaffirming an economy with robust demand for labor.

Total payroll employment is at a record 158.7 million jobs, up 6.4 million from the prepandemic high.

The unemployment rate — that is, the number of workers who identify as unemployed as a percentage of the civilian labor force — rose to 4.3% during the month. While it continues to hover near 50-year lows, the metric is now at its highest level since October 2021.

Wage growth cools. Average hourly earnings rose by 0.2% month-over-month in July, down from the 0.3% pace in June. On a year-over-year basis, this metric is up 3.6%, the lowest rate since June 2021.

Job openings fall. According to the BLS’s Job Openings and Labor Turnover Survey, employers had 8.18 million job openings in June, down from 8.23 million in May. While this remains elevated above prepandemic levels, it’s down from the March 2022 high of 12.18 million.

During the period, there were 6.81 million unemployed people — meaning there were 1.2 job openings per unemployed person. This continues to be one of the most obvious signs of excess demand for labor. However, it has returned to prepandemic levels.

Layoffs remain depressed, hiring remains firm. Employers laid off 1.5 million people in June. While challenging for all those affected, this figure represents just 0.9% of total employment. This metric continues to trend below pre-pandemic levels.

Hiring activity continues to be much higher than layoff activity. During the month, employers hired 5.34 million people.

People are quitting less. In June, 3.28 million workers quit their jobs. This represents 2.1% of the workforce, which matches the lowest level since August 2020 and is below the prepandemic trend.

A low quits rate could mean a number of things: more people are satisfied with their job; workers have fewer outside job opportunities; wage growth is cooling; productivity will improve as fewer people are entering new unfamiliar roles.

Labor productivity inches up. From the BLS: “Nonfarm business sector labor productivity increased 2.3% in the second quarter of 2024 … as output increased 3.3 percent and hours worked increased 1.0%. … From the same quarter a year ago, nonfarm business sector labor productivity increased 2.7%.

Job switchers still get better pay. According to ADP, which tracks private payrolls and employs a different methodology than the BLS, annual pay growth in July for people who changed jobs was up 7.8% from a year ago. For those who stayed at their job, pay growth was 4.8%.

Key labor costs metric cools. The employment cost index in the Q2 2024 was up 0.9% from the prior quarter, down from the 1.2% rate in Q1. This was the hottest print since Q3 2022. On a year-over-year basis, it was up 3.8% in Q2, up modestly from the 3.7% rate in Q1.

Unemployment claims rise. Initial claims for unemployment benefits increased to 249,000 during the week ending July 27, up from 235,000 the week prior. While this metric continues to trend at levels historically associated with economic growth, the latest print is the highest since August 2023.

Consumer vibes recovery stalls. The Conference Board’s Consumer Confidence Index ticked modestly higher in July. From the firm’s Dana Peterson: “Confidence increased in July, but not enough to break free of the narrow range that has prevailed over the past two years. Even though consumers remain relatively positive about the labor market, they still appear to be concerned about elevated prices and interest rates, and uncertainty about the future; things that may not improve until next year.”

More from Peterson: “Compared to last month, consumers were somewhat less pessimistic about the future. Expectations for future income improved slightly, but consumers remained generally negative about business and employment conditions ahead. Meanwhile, consumers were a bit less positive about current labor and business conditions. Potentially, smaller monthly job additions are weighing on consumers’ assessment of current job availability: while still quite strong, consumers’ assessment of the current labor market situation declined to its lowest level since March 2021.“

Weak consumer sentiment readings appear to contradict resilient consumer spending data

Consumers feel less great about the labor market. From The Conference Board’s July Consumer Confidence survey: “Consumers’ appraisal of the labor market deteriorated in July. 34.1% of consumers said jobs were “plentiful,” down from 35.5% in June. 16.0% of consumers said jobs were “hard to get,” up from 15.7%.”

Many economists monitor the spread between these two percentages (a.k.a., the labor market differential), and it’s been reflecting a cooling labor market.

From Renaissance Macro’s Neil Dutta: “Consumers spot changes in their local economies before the data. The Conference Board’s Labor Differential dropped to 18.1 in July, a fresh cycle low. Consumers are seeing softer labor market conditions and historically this has coincided with a rising unemployment rate.“

Gas prices fall. From AAA: “The national average for a gallon of gas dipped four cents since last week to $3.48. The drop comes as a tropical wave with storm-forming potential is slowly approaching the Caribbean Sea. Should it enter the Gulf of Mexico, expect oil prices to move higher.”

Card spending data is stable. From JPMorgan: “As of 22 Jul 2024, our Chase Consumer Card spending data (unadjusted) was 1.5% above the same day last year. Based on the Chase Consumer Card data through 22 Jul 2024, our estimate of the U.S. Census July control measure of retail sales m/m is 0.27%.“

From Bank of America: “Total card spending per HH was up 0.1% y/y in the week ending Jul 27, according to BAC aggregated credit & debit card data. The sectors that saw the largest improvement in spending growth since last week were department stores, transit and lodging. Gas (due to lower gas prices), online electronics and entertainment spending growth declined since last week.”

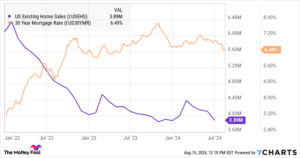

Home prices rise. According to the S&P CoreLogic Case-Shiller index, home prices rose 0.3% month-over-month in May. From S&P Dow Jones Indices’ Brian Luke: “While annual gains have decelerated recently, this may have more to do with 2023 than 2024, as recent performance remains encouraging. Our home price index has appreciated 4.1% year-to-date, the fastest start in two years. Covering the six-month period dating to when mortgage rates peaked, our national index has risen the past four months, erasing the stall experienced late last year. Collectively, all 20 markets covered continue to trade in a homogeneous pattern. Coming into the 2024 presidential election, traditional red states are in a dead heat with blue states, both averaging 5.9% gains annually.”

Mortgage rates tick lower. According to Freddie Mac, the average 30-year fixed-rate mortgage fell to 6.73% from 6.78% the week prior. From Freddie Mac: “Mortgage rates declined to their lowest level since early February. Expectations of a Fed rate cut coupled with signs of cooling inflation bode well for the market, but apprehension in consumer confidence may prevent an immediate uptick as affordability challenges remain top of mind. Despite this, a recent moderation in home price growth and increases in housing inventory are a welcoming sign for potential homebuyers.”

There are 146 million housing units in the U.S., of which 86 million are owner-occupied and 39% of which are mortgage-free. Of those carrying mortgage debt, almost all have fixed-rate mortgages, and most of those mortgages have rates that were locked in before rates surged from 2021 lows. All of this is to say: Most homeowners are not particularly sensitive to movements in home prices or mortgage rates.

Manufacturing surveys deteriorate. From S&P Global’s July U.S. Manufacturing PMI: “The manufacturing recovery moved into reverse in July, though the gloomier growth picture was accompanied by a marked cooling of inflation in the goods-producing sector. Business conditions worsened in July as the first fall in new orders since April caused a near-stalling of production. Purchasing activity is falling and hiring has slowed amid concerns over weaker-than-anticipated sales.”

Similarly, the ISM’s July Manufacturing PMI signaled contraction in the industry.

Keep in mind that during times of perceived stress, soft survey data tends to be more exaggerated than hard data.

Construction spending ticks lower. Construction spending declined 0.3% to an annual rate of $2.1 trillion in June.

Near-term GDP growth estimates remain positive. The Atlanta Fed’s GDPNow model sees real GDP growth climbing at a 2.5% rate in Q3.

Putting it all together

We continue to get evidence that we are experiencing a bullish “Goldilocks” soft landing scenario where inflation cools to manageable levels without the economy having to sink into recession.

This comes as the Federal Reserve continues to employ very tight monetary policy in its ongoing effort to get inflation under control. While it’s true that the Fed has taken a less hawkish tone in 2023 and 2024 than in 2022, and that most economists agree that the final interest rate hike of the cycle has happened, inflation still has to stay cool for a little while before the central bank is comfortable with price stability.

So we should expect the central bank to keep monetary policy tight, which means we should be prepared for relatively tight financial conditions (e.g., higher interest rates, tighter lending standards, and lower stock valuations) to linger. All this means monetary policy will be unfriendly to markets for the time being, and the risk the economy slips into a recession will be relatively elevated.

At the same time, we also know that stocks are discounting mechanisms — meaning that prices will have bottomed before the Fed signals a major dovish turn in monetary policy.

Also, it’s important to remember that while recession risks may be elevated, consumers are coming from a very strong financial position. Unemployed people are getting jobs, and those with jobs are getting raises.

Similarly, business finances are healthy as many corporations locked in low interest rates on their debt in recent years. Even as the threat of higher debt servicing costs looms, elevated profit margins give corporations room to absorb higher costs.

At this point, any downturn is unlikely to turn into economic calamity given that the financial health of consumers and businesses remains very strong.

And as always, long-term investors should remember that recessions and bear markets are just part of the deal when you enter the stock market with the aim of generating long-term returns. While markets have recently had some bumpy years, the long-run outlook for stocks remains positive.