Time to Pounce: 2 Electrifying Ultra-High-Yield Dividend Stocks That Are Begging to Be Bought in August

For well over a century, Wall Street has been rewarding patient investors. Although other asset classes have delivered positive returns, such as commodities (e.g., gold and oil), housing, and Treasury bonds, none have come close to matching the average annual return of stocks over the very long term.

But among the seemingly countless investing strategies that can be employed on Wall Street, few have fared better than buying and holding top-notch dividend stocks.

Recently, the investment advisors at Hartford Funds refreshed their data from an extensive report that examined the numerous ways dividend stocks have one-upped non-payers over multiple decades.

In particular, “The Power of Dividends: Past, Present, and Future” found that income stocks delivered an average annual return of 9.17% over the prior 50 years (1973-2023), and achieved this phenomenal return while collectively being 6% less volatile than the benchmark S&P 500. By comparison, non-payers were 18% more volatile than the S&P 500, with modest annualized returns of just 4.27% over the last half-century.

This outperformance isn’t a surprise when you consider that companies doling out a regular dividend are usually profitable on a recurring basis, time-tested, and capable of providing transparent long-term growth outlooks.

As of the closing bell on July 30, approximately 150 public companies with market caps of at least $2 billion were sporting ultra-high-yield dividends — i.e., yields that are four or more times greater than the current yield (1.36%) of the S&P 500. Among these 150 generally rock-solid businesses, there are two electrifying ultra-high-yield dividend stocks, with an average yield of 5.7%, which are begging to be bought in August.

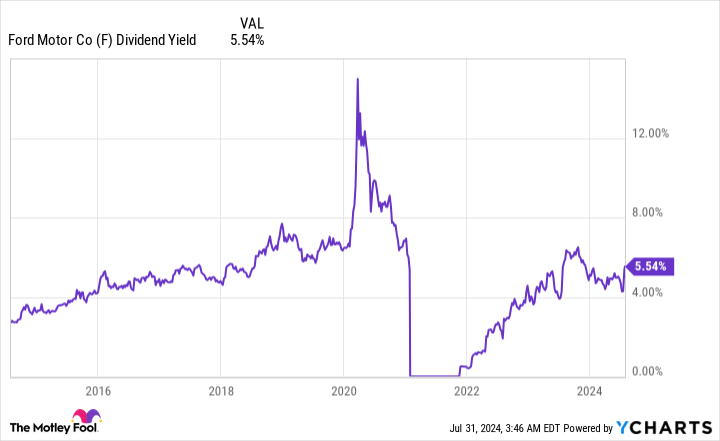

Time to pounce: Ford Motor Company (5.54% yield)

The first supercharged dividend stock opportunistic long-term investors can confidently pounce on in August is well-known automaker Ford Motor Company (NYSE: F).

Last week, shares of Ford endured their worst single day of trading in 15 years (down 18%) following the release of the company’s second-quarter operating results. Despite increasing cash flow estimates for 2024, investors cringed, once again, over the company’s high warranty-related expenses.

Automakers have also been a bit overzealous regarding an expected industrywide shift to electric vehicles (EVs). Ford’s 2024 outlook calls for Model e losses to range between $5 billion and $5.5 billion this year, with pricing pressures remaining persistent. “Model e” is the name for Ford’s EV operations.

Although the operating performance of automakers doesn’t turn on a dime, the puzzle pieces are in place for Ford to shine over the long run.

To start with, management has the flexibility to pull levers and shift spending to channels where consumer interest is high. Though the company had intended to aggressively invest in EVs, it announced plans to reduce EV spending by $12 billion last October. Until the infrastructure is in place to support EVs, and consumer sentiment shifts, focusing on the company’s highly profitable internal-combustion engine vehicles is the smarter move.

Secondly, Ford’s bread-and-butter truck segment has seen volume and pricing power remain strong. Despite all the hoopla surrounding EVs for the last couple of years, the F-Series has been the best-selling truck in the U.S. for 47 consecutive years, and the top-selling vehicle of any kind for 42 straight years. Though bigger isn’t always better, trucks generate juicier margins than small sedans, and are thus critical to Ford’s ongoing profitability.

Steadily improving the reliability of its vehicles is another core catalyst. Even though Ford is near the top of the list for recalls through the first half of 2024, my auto-focused colleague Dan Miller recently pointed out that it’s moving up the ranks of J.D. Power’s 2024 U.S. Initial Quality Study. With most of the company’s warranty issues pre-dating the hiring of current CEO Jim Farley, it looks as if Ford’s renewed focus on quality is eventually going to reduce the warranty expenses that have weighed on its operating performance.

Ford also has a healthy balance sheet that should allow it to return plenty of capital to its shareholders. The company closed out the June quarter with $20 billion in cash and cash equivalents to go along with $14.6 billion in marketable securities. Additionally, it’s expected to report a median of $8 billion in adjusted free cash flow this year. Even if things get a bit bumpy for the auto industry, Ford’s 5.5% yield appears sustainable.

The final piece of the puzzle is that Ford’s stock is reasonably cheap. The company’s forward price-to-earnings (P/E) ratio of 5.7 represents a 24% discount to its average forward earnings multiple over the trailing-five-year period.

Time to pounce: AT&T (5.85% yield)

The second electrifying ultra-high-yield dividend stock that income-seeking investors can pounce on in August is none other than telecom colossus AT&T (NYSE: T).

Though it’s fared better than Ford, AT&T’s stock has also vastly underperformed in the current bull market. One reason for this weakness is the Federal Reserve’s monetary policy. The most-aggressive rate-hiking cycle in four decades has made it costlier for companies to refinance or consummate debt-based deals. Legacy telecom companies like AT&T are carrying around quite a bit of debt.

The other concern for AT&T traces back to a July 2023 investigative report from The Wall Street Journal, which alleges that legacy telecom providers could face steep cleanup and health-related costs tied to their use of lead-clad cables.

While these are tangible headwinds that current and prospective AT&T investors shouldn’t ignore, they lack the gravity needed to really weigh on the company’s stock for an extended period.

For example, AT&T’s balance sheet has unmistakably improved since content arm WarnerMedia was spun off in April 2022. When WarnerMedia merged with Discovery to create the Warner Bros. Discovery, this new media entity assumed debt lots that AT&T had previously been responsible for. When coupled with cash payments, AT&T has reduced its net debt from $169 billion on March 31, 2022, to $126.9 billion, as of June 30, 2024. There’s no doubt that AT&T’s dividend is safe with its leverage declining.

As for the WSJ report, AT&T has refuted the findings. If there were ever to be any health-related liability claims against the company, they’d almost certainly be settled in court. The judicial process in the U.S. is slow, meaning any sort of financial liability for AT&T would be many years out. By then, its balance sheet should offer even more flexibility.

Beyond just countering headwinds, it’s important to note that AT&T is continuing to benefit from investments in its 5G network. Wireless service revenue growth is pacing around 3% for the full year, with wireless margins benefiting from an uptick in high-margin data consumption. Postpaid churn also clocked in at a historically low 0.7% in the second quarter.

Meanwhile, 239,000 AT&T Fiber net adds were logged in the June-ended quarter. This marked the 18th consecutive quarter of at least 200,000 net adds and points to the value of bringing 5G download speeds to residential homes. Broadband tends to be the lure that telecom companies use to encourage consumers to bundle their services.

Lastly, AT&T’s stock remains inexpensive at roughly 8 times forward-year earnings. Since the stock market is historically pricey, AT&T’s cheap valuation provides a safe floor that simply doesn’t exist with most stocks.

Should you invest $1,000 in Ford Motor Company right now?

Before you buy stock in Ford Motor Company, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Ford Motor Company wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $635,614!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of July 29, 2024

Sean Williams has positions in AT&T and Warner Bros. Discovery. The Motley Fool has positions in and recommends Warner Bros. Discovery. The Motley Fool has a disclosure policy.

Time to Pounce: 2 Electrifying Ultra-High-Yield Dividend Stocks That Are Begging to Be Bought in August was originally published by The Motley Fool