The ‘Trump Dump’ is back—and the stocks that he targets are crashing

A second Trump term would likely be very different from the corporate-friendly deregulatory agenda that largely defined his first.

Former President Donald Trump has long regarded the stock market as a barometer for success, constantly touting record highs during his time in office and still bragging incessantly about the “beautiful” stock market on his watch.

However, what many commentators miss is not just the 40 record highs the stock market has hit under the Biden-Harris administration—but also that while Trump does hold significant sway over pockets of the stock market, much of his impact is profoundly negative, particularly for individual companies and industries that draw his ire.

Trump’s tantrums are nothing new

Stock price moves are rarely attributable to a single factor—but there is substantial evidence suggesting that Trump’s tantrums often appear to catalyze market dislocations, especially in the companies or sectors he targets politically.

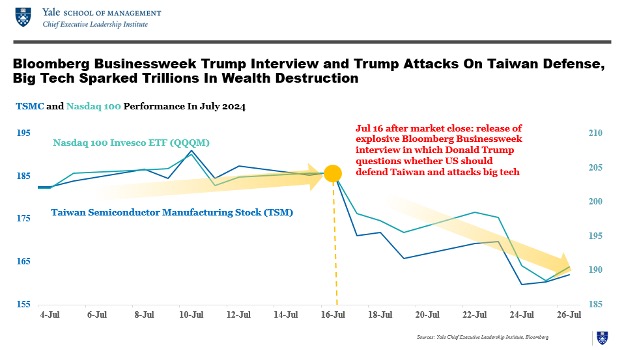

For example, consider what happened after Trump attacked Taiwan’s semiconductor manufacturers, which account for ~90% of the world’s production, and questioned whether the U.S. should defend Taiwan militarily in an interview with Bloomberg Businessweek. In the immediate aftermath, U.S.-founded Taiwan Semiconductor (TSMC) plummeted ~15%, and the broader semiconductor index plunged 10%. Charts clearly show that July 16—the date on which the Bloomberg Businessweek interview was published—was an unmistakable turning point.

In the same interview, Trump also aggressively took aim at large U.S. tech companies, exacerbating a tech sell-off, with the Nasdaq 100 falling by nearly 10% in the days after, erasing over $1.7 trillion in wealth.

Trump’s attacks on green/renewable/clean energy companies similarly sparked a rout in those specific sectors, with market commentators quipping “Trump storm batters wind and solar stocks.”

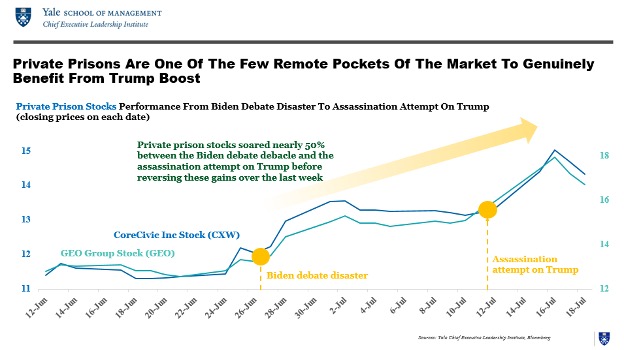

The losses in market value from Trump’s attacks dwarf the few isolated pockets of the market that have benefited significantly from the prospect of a Trump win, in what some have dubbed the “Trump Trade”—sectors that have been heavily regulated under the Biden administration, such as private prisons, predatory lenders, and gun manufacturers. In any case, initial gains in these sectors in the days following Biden’s debate disaster and the assassination attempt on Trump have largely been reversed over the last couple of weeks.

Trump crashing the stocks of companies and industries he capriciously targets is not a new phenomenon. There’s a long trail of cases dating back to his first term, when his abrupt social media pronouncements, offhand remarks, or unexpected policy shifts sank the stocks of his unfortunate targets. After all, markets generally crave predictability—the antithesis of Trump’s modus operandi.

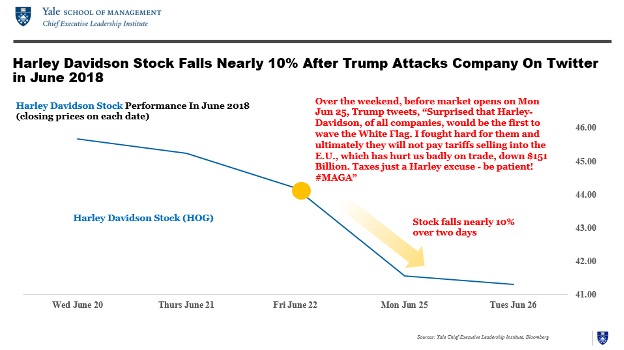

For example, Harley-Davidson dropped nearly 10% over two days in June 2018 after Trump abruptly tweeted threats to increase taxes on the company for supposedly outsourcing (which was later shown to be untrue).

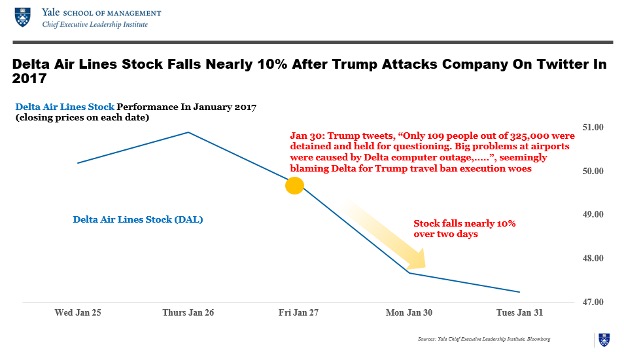

Similarly, days into his first term, the stock of Delta Airlines dropped nearly 10% over the span of two days after bizarre Trump tweets implying that the airline was to blame for the botched implementation of Trump’s travel ban and associated long delays at airports.

In other instances, companies—and their investors—were hurt by Trump’s weaponization of government to punish political enemies and help political friends.

For example, when Trump took offense at CNN’s coverage of him, he seemingly retaliated by holding up the merger between CNN’s then-parent company, Time Warner, and AT&T, for two years, hurting both badly.

And it wasn’t just individual companies or sectors. Sometimes Trump rattled the entire market with his ravings. For instance, the S&P fell 4% in two days in 2019 after Trump suddenly tweeted that he would slap tariffs on $500 billion worth of imports from China. In another case, the market lost $500 billion in value in a single day after Trump, out of nowhere, attacked Fed Chairman Jay Powell.

A Barron’s study even found that the stock market tended to fall on days when the keywords “tariffs,” “Powell,” or “Fed” showed up in Trump’s tweets. Evidently, markets did not welcome Trump’s protectionist pivots or attempts to undermine the Fed’s independence. Another study by Merrill Lynch during Trump’s first term noted that days on which Trump tweeted a lot (in the 90th percentile, defined as more than 35 tweets) were associated with statistically significant negative stock market returns.

Perilous times for the stock market

As bad as turbulence has been, a second Trump term promises to be even more perilous for the stock market. He has promised 10% tariffs on all imports and picked a running mate known for pro-antitrust, anti-corporate rhetoric. At recent rallies, Trump has started attacking the record-high stock market as just making “rich people richer,” reflecting a level of hardcore economic populism that makes even the conservative Wall Street Journal’s Editorial Board shudder. In short, a second Trump term would likely be very different from the corporate-friendly deregulatory agenda that largely defined his first.

Most importantly, the ties between Trump and America’s CEOs have frayed badly—an ominous sign given Trump’s propensity to hold personal grudges. As Bloomberg Businessweek recently reported, “Trump is highly attuned to his standing with America’s corporate chieftains… he bristles when it’s pointed out to him that no Fortune 100 CEO has publicly contributed to his campaign, according to Jeffrey Sonnenfeld in the New York Times.”

The only silver lining is that the Trump Dump usually had only a passing impact, as the targets of his taunts rebounded quickly—with the multinational firms he’s attacked as “woke” even far outperforming the “alt-right” economy and “anti-woke” startups rallying around the MAGA agenda.

However, Trump is likely to carry out his anti-corporate vendettas more efficiently and ruthlessly if he wins a second term. As Businessweek noted, “Trump believes he understands the levers of power much more deeply now…saying, ’Now, I know everybody. Now, I am truly experienced’.”

Unfettered by electoral constraints and emboldened by an improbable comeback, second-term Trump would likely extract a far steeper price on the companies that find themselves in his crosshairs—and that cost will be borne by their unfortunate shareholders.

This kind of unchecked, personalized targeting of individual companies is more typical of foreign authoritarians than anything seen in our long history. And it is no coincidence that businesses have never prospered under capricious authoritarian regimes. As one prominent GOP-supporting CEO told me, “Businesses invest where there is the rule of law, not the law of rulers.”

Trump has often tried to bend individual stocks and sectors to his will by vindictively singling them out. Investors—and all Americans—should be concerned that all the evidence points to him going even further if he wins a second term.

More must-read commentary published by Fortune:

The opinions expressed in Fortune.com commentary pieces are solely the views of their authors and do not necessarily reflect the opinions and beliefs of Fortune.