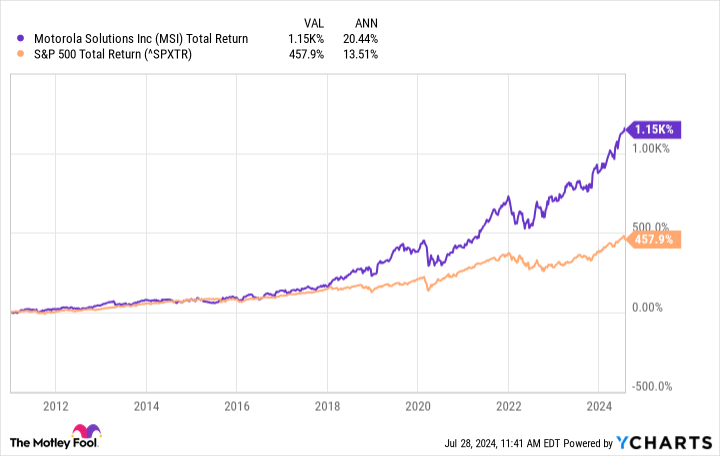

1 Magnificent S&P 500 Dividend Stock Up 1,150% Since 2011 to Buy and Hold Forever

Some stocks have total-return charts that border on the edge of being art. Posting steady returns, seemingly year in and year out, these resilient businesses are proof of the mantra, “winners keep winning.”

One company that fits this billing quite well is leading public safety and enterprise-security services provider Motorola Solutions (NYSE: MSI). Since its spinoff in 2011, Motorola has more than doubled the total returns of the S&P 500 index, consistently finding new highs time and time again.

Once more trading very near all-time highs, Motorola Solutions is ready to reach new heights yet again. Here’s what makes the company a magnificent S&P 500 dividend stock to buy and hold forever.

Motorola Solutions’ mission-critical offerings

Serving over 100,000 public safety and enterprise clients in 100-plus countries, Motorola Solutions commits to “make everywhere safer for all.” As broad and ambitious as that statement may be, Motorola does a fantastic job of delivering on this goal, operating through the three following product categories:

-

Land Mobile Radio (LMR) Communications (75% of revenue): Assisting 13,000 networks worldwide, Motorola’s rugged and “always on” LMR communications capabilities are essential for public safety departments and enterprise customers who can’t afford a lapse in coverage. For example, during disasters such as Hurricane Ian or the Maui wildfires, the company’s resilient LMR technologies allowed for crucial communication to take place when cell towers were overloaded and failing. The mission-critical nature of these solutions means that most of Motorola’s sales are incredibly sticky and recurring, as the devices in this segment tend to be updated every six to eight years.

-

Video Security and Access Control (17% of revenue): While the company has over 5 million fixed video cameras installed at 300,000 locations, Motorola’s video ambitions go far beyond just cameras and footage. With 90% of its video products containing embedded artificial intelligence (AI), the company aims to make video monitoring obsolete. Considering that humans only catch 20% of incidents within 20 minutes of happening, Motorola’s machine vision and AI capabilities have helped the company rapidly gain market share in the broader (and increasingly outdated) surveillance market. In addition to these fixed-camera solutions, the company also sells body cameras, which creates natural cross-selling opportunities with its LMR public safety and command-center customers.

-

Command Center (7% of revenue): Though it may be Motorola’s smallest segment, the command-center unit dominates its niche. With 60% of public safety answering points (911 call centers and similar emergency services) using the company’s call-handling software, Motorola is the top dog in yet another critical industry. Covering the entirety of any given emergency from detection to response to resolution, the company’s end-to-end software solutions pair beautifully with the rest of Motorola’s products to provide it with a wide switching-cost moat.

And the icing on the cake for investors? Half of Motorola’s sales come from recurring revenue tied to the software and services needed across its three product categories. These recurring sales, paired with the company’s essential products, give the company a very dependable sales base that is recession-resistant.

Top-tier cash generation funds this serial acquirer

However, just because Motorola can typically count on its customers to sign new contracts with them every few years, the company doesn’t rest on its laurels. With 8,000 of its 21,000 employees working in research and development (R&D), Motorola maintains a high R&D-to-revenue ratio of 8%, highlighting its focus on continuous innovation in safety.

Despite (or perhaps because of) this above-average spending on R&D to reinvent its products, Motorola has generated a robust free-cash-flow (FCF) margin of 16% over the last five years. The beauty of this high FCF margin is that it arms management with excess cash to use on mergers and acquisitions (M&A).

Since 2015, Motorola has spent roughly $6 billion on more than 20 acquisitions, further building out its technological prowess across all three of its product groups. Management believes these acquisitions now grow sales by more than 10% annually, generate more than $3 billion in annualized sales, and maintain an adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) margin of 20%.

Sporting a cash return on invested capital (ROIC) of 30% over the last five years, Motorola’s management has proven excellent at generating cash from the debt and equity it uses to fund its acquisitions. Historically speaking, serial acquirers like Motorola that maintain high cash ROIC have a strong tendency to beat the market, just as the company has been doing.

A premium business at a fair price

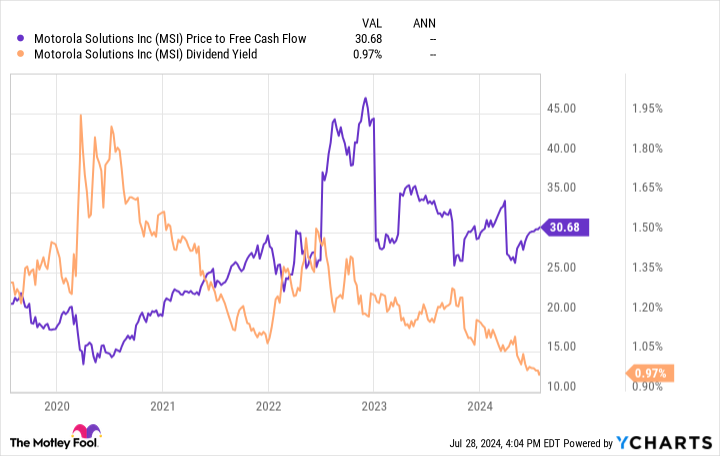

Overall, Motorola seems like a promising investment with its stellar-acquisition history, robust-cash generation, and strong positioning in its niches. However, the market has also taken notice, leaving the company to trade at 31 times FCF.

Similarly, Motorola’s dividend yield has declined to its lowest mark in over ten years despite 13 consecutive years of payout increases.

So, have investors missed their opportunity?

I don’t believe so by any means.

First, while Motorola’s yield has dipped to 1%, the company has more than quadrupled its quarterly payments since 2011, leading to an excellent 11% dividend growth rate over that time. Furthermore, despite this history of dividend increases, the company still only uses 28% of its FCF to fund these payouts, highlighting a lengthy potential runway ahead for future raises — especially considering Motorola’s resilient base of sales. Had investors bought and held shares of the company ten years ago, they would now receive a 7% yield compared to their original cost basis.

Second, thanks to management’s track record of growing through innovation from R&D and mergers and acquisitions (M&A) — and guiding for a 7% sales increase in 2024 — Motorola could be positioned for decades of “steady-Eddie” growth.

While I would be hesitant to go all in at today’s above-market valuation, Motorola Solutions looks to be a classic example of a premium dividend-growth stock trading at a fair price, making it perfect for dollar-cost-averaging purchases over time.

Should you invest $1,000 in Motorola Solutions right now?

Before you buy stock in Motorola Solutions, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Motorola Solutions wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $657,306!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of July 29, 2024

Josh Kohn-Lindquist has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

1 Magnificent S&P 500 Dividend Stock Up 1,150% Since 2011 to Buy and Hold Forever was originally published by The Motley Fool